國債超過21萬億,,特朗普該怎么辦,?

|

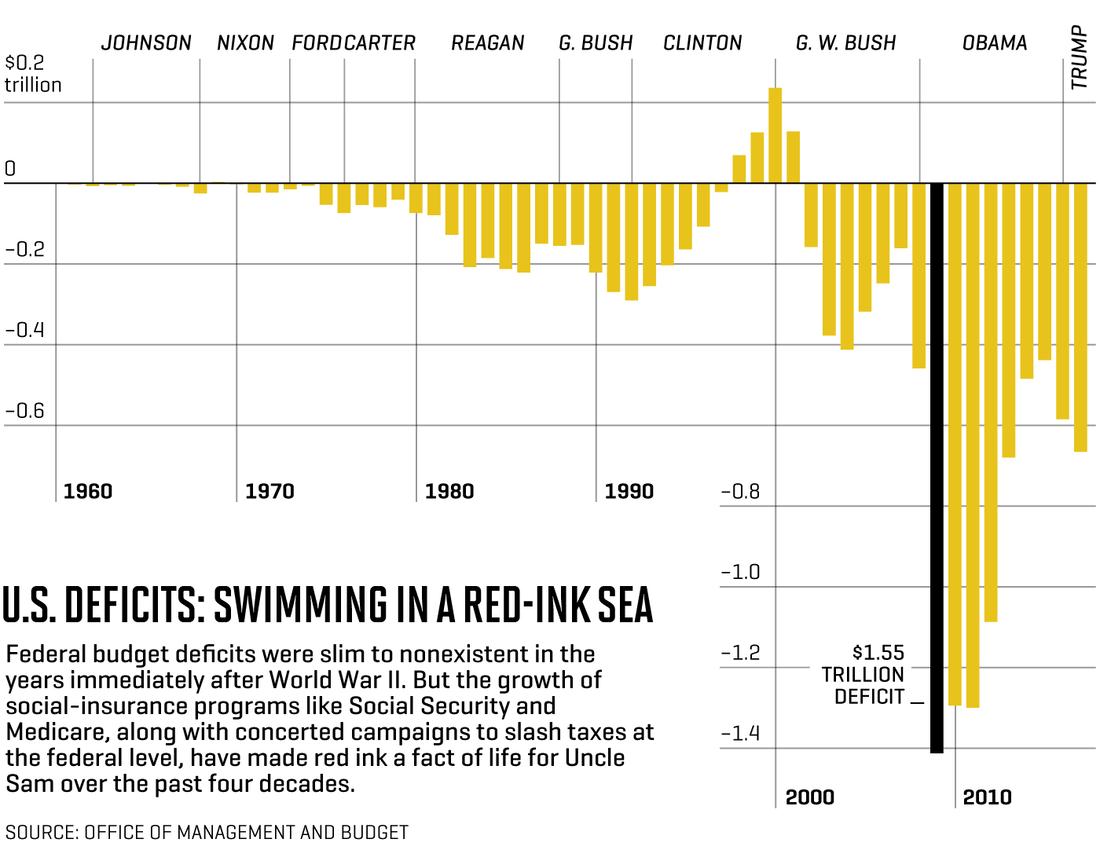

唐納德·特朗普宣稱,也只有唐納德·特朗普能夠如是宣稱,,美國經(jīng)濟(jì)的強(qiáng)勁復(fù)蘇正在推動美國走向新的輝煌,,而他正是這一切的促成者。這位總統(tǒng)在最近一篇具有代表性的推文中斷言,,“如今,,我們的經(jīng)濟(jì)一片繁榮,而且,,得益于我所做的一切,,美國經(jīng)濟(jì)定會扶搖直上……美國即將再次立于不敗之地!” 雖然“繁榮”一詞是特朗普式的夸耀之詞,,但不可否認(rèn)的是,,從眾多方面來看,這位總統(tǒng)的政策事實上取得了巨大的成功,。在特朗普入主白宮整整三個季度之際,,美國GDP增速僅僅略低于他所承諾的3%的目標(biāo)。按照近些年的標(biāo)準(zhǔn)來衡量,,這一成績實屬驚艷,。股市市值自特朗普當(dāng)選之后增長了四分之一,相當(dāng)于5萬億美元的獻(xiàn)禮,。這一欣欣向榮的前景也重振了企業(yè)領(lǐng)袖的擴(kuò)張野心:在其1月對中小企業(yè)的調(diào)查中,美國獨立企業(yè)聯(lián)合會發(fā)現(xiàn),,32%的企業(yè)認(rèn)為當(dāng)前是“擴(kuò)張的好時機(jī)”,。這一比例可謂是創(chuàng)下了新的記錄,,同時也較2016年底翻了三番。 我不日將前往瑞士達(dá)沃斯,,向全世界宣揚美國的偉大之處,,以及美國的近況。如今,,我們的經(jīng)濟(jì)一片繁榮,,而且,得益于我所做的一切,,美國經(jīng)濟(jì)定會扶搖直上……美國即將再次立于不敗之地,! 特朗普標(biāo)志性的立法成就——《減稅與就業(yè)法案》——更是為這一政績錦上添花。該法案將企業(yè)所得稅率從35%減為21%,。新法案讓企業(yè)領(lǐng)袖喜出望外,,包括美國航空、沃爾瑪和Verizon在內(nèi)的各大公司均預(yù)測這一舉措將使公司未來的盈利大增,。大型企業(yè)首席執(zhí)行官,,從摩根大通的杰米·戴蒙到波音的丹尼斯·穆倫伯格,一致稱贊其是美國競爭力的強(qiáng)效補(bǔ)劑,。即將到來的利潤激增已促使200多家《財富》500強(qiáng)企業(yè)提升其最低薪酬(美國銀行,、哈門那等公司),或向員工發(fā)放一次性獎金(家得寶,、迪士尼等公司),,或兩者兼而有之。 然而,,特朗普令人目眩神迷的經(jīng)濟(jì)補(bǔ)劑將掩蓋那些錯誤的政策,,從而讓這些企業(yè)在一時的歡愉之后出現(xiàn)嚴(yán)重的后遺癥。美國政府大量不斷增長的預(yù)算赤字已成為了一個龐然大物,,足以威脅偉大的美國增長機(jī)器,。同時,特朗普到目前為止祭出的大幅稅收削減和開支劇增的組合政策,,將大幅擴(kuò)大收支之間不可持續(xù)的鴻溝,,并縮短財政定時炸彈的導(dǎo)火索。按照當(dāng)前的態(tài)勢,,等待我們的將是充斥著懲罰性稅收,、增長乏力和工人薪資停滯不前的亂攤子,與特朗普所宣稱的未來恰恰相反,。 到2028年,,美國政府債務(wù)負(fù)擔(dān)可能會從今年的15.5萬億美元激增至33萬億美元,對比特朗普的減稅法案未得到通過的未來債務(wù)水平,,增幅超過了20%,。到那時,,利息支出將消耗超過20%的聯(lián)邦收入,政府也就無力促進(jìn)經(jīng)濟(jì)發(fā)展,,并控制私營領(lǐng)域,。與總統(tǒng)和其支持者的聲稱背道而馳的是,美國經(jīng)濟(jì)的增速還達(dá)不到擺脫這一債務(wù)負(fù)擔(dān)的水平,;不但如此,,特朗普在移民和貿(mào)易方面的舉措看起來可能會對經(jīng)濟(jì)增長起反作用。(下文會詳細(xì)說明,。)穆迪分析的首席經(jīng)濟(jì)師馬克·贊迪表示,,“此舉就像是氣候變化一樣。短時間內(nèi)看不到什么影響,,但一旦那一天真的來臨,,人們才能真正認(rèn)識到這些政策的弊端?!? 由于沒有采取果斷,、迅速的行動來應(yīng)對這一滯后型危機(jī),未來幾年內(nèi)最樂觀的情形是,,美國將成為一個風(fēng)險頗高的經(jīng)商地,。大量的債務(wù)將限制美國保持經(jīng)濟(jì)平衡發(fā)展的可用手段。哈佛大學(xué)經(jīng)濟(jì)學(xué)家肯尼斯·羅格夫表示,,“債臺高筑的國家對于經(jīng)濟(jì)下行不會采取激進(jìn)的應(yīng)對措施,。”如果美國陷入衰退,,我們將失去減稅或提升基礎(chǔ)設(shè)施建設(shè)投入的機(jī)會,,例如,將其作為重振增長的工具,。而且隨著債務(wù)負(fù)擔(dān)的加重,,美聯(lián)儲刺激經(jīng)濟(jì)的降息舉措更有可能會讓通脹失去控制?!澳菚r,,投資者將拋售美國國債”,胡佛研究所經(jīng)濟(jì)學(xué)家約翰·柯克蘭說道,,“這會導(dǎo)致利率大漲,,同時讓預(yù)算問題更加嚴(yán)重?!? 剛退休的霍尼韋爾首席執(zhí)行官大衛(wèi)·科特指出,,華盛頓方面到如今依然對這一即將到來的災(zāi)難視而不見,這一現(xiàn)象將讓企業(yè)領(lǐng)導(dǎo)者感到異常擔(dān)憂。2010年,,科特曾供職于辛普森-鮑勒斯委員會,,它是一個由18名成員組成的部門,受命為美國尋找可持續(xù)的財政出路,。雖然委員會平臺未能在國會中存活下來,但其在提升營收以及醫(yī)療和社保改革方面的平衡舉措得到了人們的稱贊,??铺胤Q,即便這一問題在如今已經(jīng)無比嚴(yán)重,,但決策者們卻在自掘更深的墳?zāi)?。科特對《財富》說,,“我們在辛普森-鮑勒斯委員會中花了頗大的氣力才與兩黨談妥社會福利改革和增稅問題,。”他還提到,,在大蕭條之前,,美國債務(wù)占GDP的比重為35%。今冬,,美國的債務(wù)增長了一倍多,,科特感慨道,“特朗普總統(tǒng)和國會同意減稅并提升開支,。我害怕這只是一種破罐子破摔的行為,。” |

Donald Trump is pitching, as only Donald Trump can pitch, that a major economic revival is energizing America for a new run at greatness, and that he’s the straw stirring the elixir. In one representative recent tweet, the President declared, “Our economy is now booming and with all I am doing, will only get better?…?Our country is WINNING again!” Though “booming” is Trumpian overstatement, it’s undeniable that by many criteria, the President’s agenda is proving remarkably successful. In Trump’s first three full quarters in the White House, GDP clocked growth just shy of his vaunted goal of 3%, a performance that by recent standards looks stellar. The stock market has added a quarter to its value since the election, a $5 trillion vote of confidence. The jaunty outlook is recharging animal spirits in corner offices: In its January survey of small companies, the National Federation of Independent Business found that 32% of the enterprises rated the present climate “a good time to expand”; that was a record high and a threefold increase from late 2016. Donald J. Trump?@realDonaldTrump Will soon be heading to Davos, Switzerland, to tell the world how great America is and is doing. Our economy is now booming and with all I am doing, will only get better...Our country is finally WINNING again! 8:27 AM - Jan 25, 2018 Fueling the giddiness is the President’s signature legislative achievement: the Tax Cuts and Jobs Act, which slashed rates for corporations from 35% to 21%. The new law is a runaway hit with business leaders. Companies as varied as American Airlines , Walmart , and Verizon predict that the measure will swell their earnings for years to come, and marquee CEOs from JPMorgan Chase’s Jamie Dimon to Boeing’s Dennis Muilenburg laud it as a powerful tonic for American competitiveness. The looming profit surge has prompted more than 200 Fortune 500 companies to raise their minimum pay (U.S. Bancorp, Humana), issue one-time bonuses to employees (Home Depot, Walt Disney), or both. Trump’s heady economic potion, however, is masking misguided policies that could leave those same businesses with a severe hangover from today’s celebration. The U.S. government’s huge and growing budget deficits have become gargantuan enough to threaten the great American growth machine. And Trump’s policies to date—a combination of deep tax cuts and sharp spending increases—are shortening the fuse on that fiscal time bomb, by dramatically widening the already unsustainable gap between revenues and outlays. On our current course, we’re headed for a morass of punitive taxes, puny growth, and stagnant incomes for workers—a future that’s the precise opposite of what Trump champions. By 2028, America’s government debt burden could explode from this year’s $15.5 trillion to a staggering $33 trillion—more than 20% bigger than it would have been had Trump’s agenda not passed. At that point, interest payments would absorb more than $1 in $5 of federal revenue, crippling the government’s ?capacity to bolster the economy, and constraining the private sector too. Contrary to the claims of the President and his supporters, the U.S. can’t grow fast enough to shed this burden; indeed, Trump’s agenda on immigration and trade looks likely to stunt that growth. (More on that later.) “This is almost like climate change,” says Mark Zandi, chief economist at Moody’s Analytics. “It doesn’t do you in this year, or next year, but you’ll see the ill effects in a day of reckoning.” In the absence of decisive, quick action to tackle this slow-motion crisis, the best-case scenario for the next few years is that America becomes a much riskier place to do business. A high debt load will limit our flexibility to keep the economy on an even course. “Countries with high debt don’t respond aggressively to downturns,” says Harvard economist Kenneth Rogoff. If the U.S. slips into recession, we’ll lack the option of lowering taxes or increasing spending on infrastructure, for example, as tools to revive growth. And as the debt load grows, efforts by the Federal Reserve to stimulate the economy with lower rates would be more likely to feed runaway inflation. “Then, investors will dump Treasuries,” says John Cochrane, an economist at the Hoover Institution. “That will drive rates far higher, and make the budget picture even worse.” For now Washington is neglecting the coming crunch, and that should make business leaders plenty worried, says David Cote, the recently retired CEO of Honeywell (HON, +0.44%). In 2010, Cote served on the Simpson-Bowles Commission, an 18-member group charged with finding ways to put America on a sustainable fiscal path. Though the commission’s platform died in Congress, it drew praise for its balanced approach to raising revenues and reforming Medicare and Social Security. Cote says that even though the problem is far more dire today, policymakers are digging a deeper hole. “We made a grand, bipartisan bargain in Simpson-Bowles to reform entitlements and raise taxes,” Cote tells Fortune, noting that prior to the Great Recession, the ratio of debt to GDP was 35%. This winter, with debt more than twice as high, marvels Cote, “President Trump and Congress agreed to reduce taxes and raise spending. I’m afraid that people are just giving up.” |

|

科特警告說,首席執(zhí)行官們不應(yīng)慶祝,,而是應(yīng)針對風(fēng)險超高的未來做好規(guī)劃,,屆時不斷惡化的金融環(huán)境可能會讓其利潤受到嚴(yán)重打擊。其中一個危險在于,,因債務(wù)劇增和控制舉措缺失而有所警覺的外國投資者可能會拋售美國債券,,進(jìn)而推高利率??铺卣f:“利率每升高1個百分點,,債務(wù)每年就會增加2000億美元?!笔找媛实募ぴ鲆矔嵘T檻,,屆時新投資會獲利,這將迫使公司緊縮開支,。 企業(yè)高管可能還會擔(dān)心,,解決債務(wù)問題的唯一辦法就是提高稅率,。科特說:“此舉會對企業(yè)對投資環(huán)境的看法帶來巨大的影響,。各大企業(yè)將變得憂心忡忡,,并撤回投資,轉(zhuǎn)而觀望,?!钡J(rèn)為,觀望會導(dǎo)致增長停滯和惡化,。這種停滯不前會讓特朗普第一年的經(jīng)濟(jì)改觀轉(zhuǎn)瞬即逝,。 當(dāng)然,美國財政格局遠(yuǎn)在特朗普上任之前便失去了其可持續(xù)性,。不過,,真正令人感到震驚的是,特朗普的稅收削減和開支增加政策竟會讓這一格局的前景變得如此的暗淡,,而且是如此地迅速,。 此舉對經(jīng)濟(jì)增長的威脅來自于兩個方面。首先,,美國一直以來對于老年人頗為照顧,,而且對窮人亦是不吝幫扶,福利模式與歐洲相當(dāng),,但美國卻通過舉債來資助這些項目,,而不是采取歐洲式的高稅收政策。此舉可謂是政路亨通:在去年4月的民調(diào)中,,皮尤研究中心詢問選民是否支持14個特定預(yù)算領(lǐng)域的開支削減,。大多數(shù)民主黨人士反對對任何預(yù)算進(jìn)行削減,而共和黨人士同意削減其中的一項,,即“向全球受難民眾提供協(xié)助,。” 這一點也引出了第二個方面,。與財政改革完全相悖的兩個法案既得到了特朗普的支持,,也得到了國會的批準(zhǔn)。 國會的稅務(wù)聯(lián)合委員會稱,,即便12月簽署的稅收削減法案會提振增長和收入,,但它也會讓美國的預(yù)期財政收入在未來10年內(nèi)減少1萬億美元,也就是每年1000億美元,。得出這一結(jié)果的前提是,,大多數(shù)個人所得稅削減將在8年內(nèi)到期,而且資本設(shè)備費用化減稅將在2023年逐漸停止。保守派曼哈頓研究生的布萊恩·瑞德爾表示,,“這些減稅非常有可能得以延期,。”他預(yù)測,,在減稅延期有望的環(huán)境下,,這項減稅法案將導(dǎo)致財政收入在接下來的10年中減少1600億美元。 同時,,2月份的聯(lián)邦預(yù)算議案顯示,,可自由支配開支項下的兩個門類——國防和聯(lián)邦支出(從外國援助到房屋補(bǔ)貼)——的費用均出現(xiàn)了12%的增長,也就是2018年,、2019年每年增長1500億美元,這是史無前例的,。它基本上取消了2011年預(yù)算控制法案所設(shè)定的兩黨開支上限,,而這一法案也讓近期赤字多少受到了一些控制。上述開支增長在國會中受到了兩黨的熱烈歡迎,,而且?guī)缀醣厝粫_啟一個新的預(yù)算開支平臺,,未來開支在此基礎(chǔ)上必然會有所增加。 瑞德爾估計,,稅收削減和開支增加每年將帶來共計約3750億美元的赤字,,包括新增的利息。財政方面的應(yīng)對舉措本應(yīng)是尋找提振收入的手段,,并減少其他預(yù)算領(lǐng)域的開支,,以彌補(bǔ)這一缺口。然而,,盡管法案提到了一些抵消手段,,但這些手段在鋪天蓋地的減稅面前卻又是那么微不足道。 去年6月,,國會預(yù)算辦公室預(yù)測,,赤字將在2022年達(dá)到1萬億美元。非黨派機(jī)構(gòu)負(fù)責(zé)人聯(lián)邦預(yù)算委員會稱,,由于新稅收法案的出臺,,如果當(dāng)前的稅收和開支政策繼續(xù)得以延續(xù),美國赤字突破這一門檻的時間將大幅提前至2019年,。即便經(jīng)濟(jì)繁榮發(fā)展,,那些可能出現(xiàn)的資金缺口將繼續(xù)擴(kuò)大。根據(jù)國會預(yù)算辦公室的預(yù)測,,如果沒有減稅法案,,赤字將在2028年達(dá)到約1.6萬億美元。如今,聯(lián)邦預(yù)算委員會預(yù)測會出現(xiàn)2.4萬億美元的缺口,。美國在接下來的10年中所支出的三分之一資金都將是借來的,,這在很大程度上歸咎于上述擴(kuò)大赤字的舉措。如果開支和收入如以前那樣沒有什么變化,,那么這一比例將變成四分之一,。 10年后,聯(lián)邦債務(wù)水平將達(dá)到觸目驚心的33萬億美元,,相當(dāng)于GDP的113%,,較稅收削減法案出臺之前國會預(yù)算辦公室預(yù)測的數(shù)字高出了6萬億美元。美國借貸的利息也將成為聯(lián)邦預(yù)算中增速最快的開支項目,,它的增幅將超過2倍,,每年接近1.1萬億美元。到那時,,債務(wù)持有成本將相當(dāng)于醫(yī)療支出的一半,。如果通脹或利率超過了國會預(yù)算辦公室所預(yù)測的相對較低的門檻值,利息賬單甚至?xí)兊酶佑|目驚心,。聯(lián)邦預(yù)算委員會的高級政策理事馬克·戈爾德文指出,,“這一增幅就是美國扔掉的錢,相當(dāng)于占用了可用于醫(yī)療,、軍事等眾多項目的資金,。” 這種占用會帶來切實的影響,。償還飆升債務(wù)所需的成本會給政府帶來巨大的壓力,,迫使政府取消可用于刺激經(jīng)濟(jì)增長的投資。在過去,,用于修繕高速公路,、公交系統(tǒng)或用于改善高等教育的開支曾提升了美國勞動力的生產(chǎn)力。這些開支提升了民眾收入,,推高了儲蓄率,,刺激了消費支出,并增加了可用于私人投資的儲蓄,。迅速增長的債務(wù)所帶來的利息負(fù)擔(dān)會將這一良性循環(huán)變成一個難以維繼的海市蜃樓,。 政府是否會在財政危機(jī)或遠(yuǎn)超警戒線的赤字增幅發(fā)生之前采取糾正性對策,這一點我們無法斷言,。穆迪投資者服務(wù)的高級副總裁薩拉·卡爾森表示,,可以肯定的是,“我們等的時間越長,,福利削減和稅收增加的舉措就越難開展,?!? 然而,正如科特所提到的那樣,,決策者并沒有意愿采取那些不怎么受歡迎而且可能十分激進(jìn)的舉措,,并借此重塑美國財政平衡。2月9日,,參議院就提升可自由支配開支進(jìn)行了投票,,期間,共和黨預(yù)算鷹派(像肯塔基州蘭德·保爾和猶他州麥克·李)的反對之聲被34名共和黨參議員和上院36名民主黨參議員所淹沒,,最終通過了這一助長赤字的議案,。這一跡象表明,國會已經(jīng)將審慎財政政策拋之腦后,。特朗普也不大可能去填補(bǔ)這一財政責(zé)任深坑:這位總統(tǒng)在其5866字的國情咨文中對財政“赤字”或“債務(wù)”只字未提,。 有一種方法可以讓美國繼續(xù)保持現(xiàn)狀,那就是繼續(xù)肆無忌憚地向世界各國借錢,。美國之所以一直能夠揮霍度日,,原因在于外國借貸者對美國政府和企業(yè)債務(wù)有著濃厚的興趣。在當(dāng)前美國的15.5萬億美元的債券中,,他們?nèi)缃癯钟衅渲械?萬億美元。 對于大多數(shù)國家來說,,這類大規(guī)模借貸會推高利率,,因為政府將與企業(yè)競爭有限的借貸資金池。但是幾十年以來,,美國并未出現(xiàn)這樣的情況:來自于全球各地,,包括中國、日本和其他海外投資者的大量資金抑制了利率的增長,。如今,,美國是全球最強(qiáng)大的多元化企業(yè)經(jīng)濟(jì)體,而且在全球經(jīng)濟(jì)不景氣的環(huán)境下,,資金會涌入最安全的安全港——美國,。唯一得到大蕭條證實的一條理論是:“我們向世界輸出了金融危機(jī),而世界卻向我們提供了資金,?!保ǔ鲎杂诩又荽髮W(xué)伯克利分校經(jīng)濟(jì)學(xué)家阿蘭·歐拉巴克)。 這位總統(tǒng)在其5866字的國情咨文中對“赤字”或“債務(wù)”只字未提,。 但據(jù)此設(shè)想世界會對美國的揮霍無度繼續(xù)聽之任之將會是一個高風(fēng)險賭注,,同時,如果國會依然對未來十年應(yīng)采取的痛苦抉擇視而不見,,其風(fēng)險會變得更高,。發(fā)生2010年希臘式的全面崩潰——經(jīng)濟(jì)放緩,,懲罰性利率,迫使當(dāng)局采取改革措施——的可能性到是不大,。更為可能的情形是,,年度債務(wù)數(shù)字變得異常糟糕,并引起了世界各國的關(guān)注,,然后即將到來的赤字懸崖再次成為了一個重大的政治問題,。美國人可能會因為巨大的預(yù)算赤字而變得憤怒不已:上個世紀(jì)80年代的過度赤字所產(chǎn)生的赤字焦慮促使兩黨達(dá)成共識——在1990年布什總統(tǒng)首次入主白宮時提升稅收并縮減赤字。 周期的下行,,股價的大幅下跌或由多疑的海外投資者所引發(fā)的始料未及的真實利率大幅上升,,或許會成為促使立法者開始認(rèn)真對待赤字的催化劑。上述現(xiàn)象不會帶來災(zāi)難,,但是通過降低財政收入或擴(kuò)大已經(jīng)觸目驚心的赤字,,它會引導(dǎo)人們聚焦可能成為現(xiàn)實的災(zāi)難性未來。戈爾德文說:“決策者們將制定一些在眼下不需要大量資金,、但卻能夠逐漸顯現(xiàn)成效的方案,。”換句話說,,他們會讓美國進(jìn)入下滑通道,,以重拾市場信心。 |

Rather than celebrating, Cote warns, CEOs should be planning for an ultra-risky future where the worsening financial climate could cut deep into their profits. One danger is that foreign investors, alarmed both by our crushing debt and the absence of plans to tame it, could dump our Treasuries, pushing interest rates higher. “A one point rise in rates adds $200 billion every year to the debt,” says Cote. A jump in yields would also raise the threshold at which new investments become profitable, forcing companies to retrench. Corporate leaders may also fret that the only solution to our debt woes is a jolting rise in taxes. “That would have a huge impact on how businesses view the investment climate,” Cote says. “Companies will get worried and pull back on investment and wait and see.” But to wait and see, he predicts, is to court stagnation and deterioration. That kind of stasis would turn the good economic news of President Trump’s first year into a short story. Of course, America’s fiscal picture was becoming unsustainable well before Trump took office. What’s astounding is how much worse his tax cuts and spending increases have rendered the outlook, and how quickly. The causes of this menace to prosperity are twofold. First, the U.S. has long chosen to lavish seniors, and to a lesser extent support the poor, with European-style benefits, while borrowing to fund those programs rather than levying European-style taxes. It’s a politically popular path: In a poll released last April, the Pew Research Center asked voters whether they supported spending reductions to 14 specific budget areas. A majority of Democrats opposed cuts to any, while Republicans endorsed shrinking just one, “assistance to needy people around the world.” That brings us to the second point. Trump has championed, and Congress has enacted, two laws that go in the opposite direction of fiscal reform. According to Congress’s Joint Committee on Taxation, the Tax Cuts act, signed in December, will decrease expected revenues by a total of $1 trillion over the next 10 years, an average of $100 billion annually, even after any boost to growth and incomes from lower taxes. That number assumes that most of the personal income-tax reductions expire in eight years, and a break for expensing capital equipment starts phasing out in 2023. “Those breaks are extremely likely to be renewed,” says Brian Riedl of the conservative Manhattan Institute—and in that more likely scenario, he projects, the tax plan will lower revenues by $160 billion over the following decade. The February federal budget deal, meanwhile, hikes outlays in both of the two categories of “discretionary” spending, defense and federal programs from foreign aid to housing subsidies, by an unprecedented 12%, or $150 billion a year in 2018 and 2019. It essentially obliterates bipartisan spending caps established in the Budget Control Act of 2011 that had kept recent deficits partially in check. These spending increases are so popular on both sides of the congressional aisle that they’re almost certain to establish a new floor for discretionary spending, from which future expenditures will rise. All told, the tax cuts and increased spending will raise deficits by roughly $375 billion annually, by Riedl’s estimates, including additional interest. The fiscally responsible path would have been to enact revenue-raisers and spending curbs elsewhere in the budget to fill the gaps. But although the tax bill included some offsets, they were swamped by the sweeping reduction in taxes. Last June, the Congressional Budget Office (CBO) forecast that deficits would reach $1 trillion in 2022. Because of the new laws, America will exceed the $1 trillion mark much earlier, in 2019, assuming current tax and spending policies are extended, according to the nonpartisan Committee for a Responsible Federal Budget (CRFB). Those probable shortfalls will keep ballooning even if the economy thrives. Under the CBO’s forecast, deficits would have reached roughly $1.6 trillion in 2028 without the new laws. Now, the CRFB predicts a shortfall of $2.4 trillion. Largely owing to the deficit-widening measures, the U.S. in a decade will borrow $1 in every $3 it spends, vs. $1 in $4 if outlays and revenues had remained on their prior path. In a decade, federal debt will reach an overwhelming $33 trillion, the equivalent of 113% of GDP—and $6 trillion higher than the CBO had forecast before the Trump agenda passed. Interest on U.S. borrowings would become the fastest-growing item in the federal budget, more than tripling to almost $1.1 trillion annually. At that point, carrying costs would equal one-half of spending on Medicare, and if inflation or interest rates exceeded the relatively low thresholds in the CBO’s forecasts, the interest bill would soar even higher. “That increase represents money the U.S. is just throwing away—that’s crowding out the funding on everything from health care to the military,” says Marc Goldwein, the CRFB’s senior policy director. That crowding out has real consequences. The cost of servicing the exploding debt would exert tremendous pressure on the government to eliminate investments that could fuel growth. In the past, spending that modernized highways and mass-transit systems or enhanced higher education has boosted the productivity of America’s workers. That raises incomes, boosts savings rates, lifts consumer spending, and swells savings that fund private investment. The interest burden generated by the mushrooming debt threatens to turn this virtuous cycle into an unaffordable luxury. It’s impossible to say whether a fiscal crisis, or growing outrage over the alarming numbers, might prompt corrective action before that happens. What’s certain, says Sarah Carlson, a senior vice president at Moody’s Investors Service, is that “the longer we wait, the tougher the choices on benefits cuts and tax increases become.” Yet as Cote points out, policymakers are showing no willingness to take the unpopular, potentially radical steps needed to restore America’s fiscal balance. A sign of just how far Congress has shifted away from fiscal caution is the Senate vote on Feb. 9 to raise discretionary spending: Opposition from Republican budget hawks such as Rand Paul of Kentucky and Mike Lee of Utah was overwhelmed by the 34 GOP Senators who joined 36 Democrats in the upper chamber to pass the deficit-swelling measure. Nor is Trump likely to fill the fiscal-responsibility vacuum: The President failed to even mention fiscal “deficits” or “debt” a single time in his 5,866-word State of the Union Address. There is one scenario in which the U.S. could stay on its current course, and that’s to keep blithely borrowing from the rest of the world. America has been able to play the spendthrift because foreign lenders have shown a huge appetite for both our government and corporate debt—they now own $6 trillion of our $15.5 trillion in publicly owned Treasuries. For most nations, such colossal borrowings would push interest rates higher as the government competes with business for a limited pool of lendable assets. But for decades, that hasn’t been the case for the U.S.: A worldwide glut of savings from Chinese, Japanese, and other overseas investors holds our rates in check. The U.S. is, for now, the world’s most powerful, well-diversified, and entrepreneurial economy, and in times of global stress, ?money pours into the safest of all safe havens, the United States. The Great Recession only proved the thesis. “We exported a financial crisis to the rest of the world, and they sent us their money,” says UC–Berkeley economist Alan Auerbach. The president failed to even mention “deficits” or “debt” a single time in his 5,866-word state of the Union address. But assuming that the rest of the world will continue to turn a blind eye to American profligacy is a risky bet, and it will get riskier if Congress keeps skirting the tough choices for the next 10 years. A full-blown Greece-in-2010-style debacle—a slowdown of the economy, coupled with punitive interest rates, that forces major reforms—is faintly possible but unlikely. A more probable plotline involves a scenario in which the annual debt numbers become so bad, and draw so much attention, that our looming fiscal cliff once again becomes a major political issue. Americans can get riled over gigantic budget deficits: Deficit anxiety after the excesses of the 1980s prompted a bipartisan deal to raise taxes and shrink deficits under the first President Bush in 1990. A cyclical downturn, a sharp decline in stock prices, or an unexpectedly steep increase in real interest rates dictated by skeptical overseas investors might be the catalyst that prompts legislators to get serious. It wouldn’t cause catastrophe, but by lowering revenues or widening the already yawning deficits, it would train the spotlight on the potentially disastrous outlook. “Policymakers would form plans that wouldn’t need to raise tons of money right now, but would kick in gradually,” says Goldwein. In other words, they’d shift the U.S. to a glide path that would reassure the markets. |

一場危機(jī)引發(fā)另一場危機(jī):大蕭條期間和之后政府的買單行為和一落千丈的稅收為第一財務(wù)部長提摩西·哥特內(nèi)帶來了1萬億多美元的赤字,。Josua Robert—Bloomberg via Getty Images

|

特朗普政府認(rèn)為,這類舉措并非是當(dāng)前的重點,,因為經(jīng)濟(jì)增長會消化掉其中的很多問題,。財政部長史蒂芬·姆努欽在去年稱,“通過稅收改革和放松監(jiān)管,,美國可以獲得更高的GDP增速,,有助于消除國家的財政赤字?!钡饨绾苌儆腥苏J(rèn)為美國能夠?qū)崿F(xiàn)特朗普和姆努欽所稱的3%的增長目標(biāo),。國會預(yù)算委員會、經(jīng)合組織和世界銀行均預(yù)測,,美國未來10年的增速約為2%,。主要原因在于:美國人口的老齡化導(dǎo)致勞動力增速的下降,。 此外,有鑒于特朗普在經(jīng)濟(jì)政策領(lǐng)域所采取的非常難以預(yù)測,、非常矛盾的方法,,經(jīng)濟(jì)增速能否達(dá)到2%都是一個問題。特朗普所支持的立法出臺后,,美國每年的合法移民數(shù)量在未來10年內(nèi)將降低50%,。房利美首席經(jīng)濟(jì)師道格·鄧肯指出,“說到對增長的限制,,控制移民可謂是最直接的方式,。”鄧肯認(rèn)為,,外國勞動力所創(chuàng)辦的企業(yè)要比美國人多得多,,而且美國需要他們來避免出現(xiàn)可能會造成嚴(yán)重后果的行業(yè)勞動力短缺,包括農(nóng)業(yè),、建筑和科技,。特朗普還在推行他的商業(yè)支持者希望其拋棄的手段:利用關(guān)稅來打壓進(jìn)口。特朗普首先做的便是對外國制造的鋼鐵和鋁制品征收高額關(guān)稅,。穆迪的贊迪說:“關(guān)稅會拉高美國制造商使用這些材料的價格,,并放緩銷售和投資?!? |

The Trump administration argues that such maneuvers aren’t a high priority, because economic growth will solve a lot of the problem. “Through a combination of tax reform and regulatory relief, this country can return to higher levels of GDP growth, helping to erase our fiscal deficit,” Treasury Secretary Steven Mnuchin declared late last year. But few outside the administration believe that America can expand at the 3% rate that Trump and Mnuchin are targeting. The CBO, Organization for Economic Cooperation and Development (OECD), and World Bank all forecast an average reading of around 2% over the next decade. A major reason: a decline in the rate of workforce growth because of our aging population. What’s more, Trump’s highly unpredictable, and highly contradictory, approach to economic policy makes even 2% growth uncertain. Trump supports legislation that would reduce the annual number of legal immigrants by 50% over 10 years. “There’s no more direct way to cut growth than restricting immigration,” says Doug Duncan, chief economist at Fannie Mae. Duncan notes that foreign workers both start far more businesses than Americans, and that they’re needed to avoid potentially crippling labor shortages in industries from farming to construction to tech. Trump is also delivering on what his business supporters hoped he’d abandon: deploying tariffs to punish imports, starting with heavy duties on foreign-made steel and aluminum. “Tariffs raise prices for U.S. manufacturers using those materials, and slow sales and investment,” says Moody’s Zandi. |

|

雖然特朗普的稅收和監(jiān)管立場在短期內(nèi)十分親商,但這些政策是經(jīng)濟(jì)增長的殺手,。最致命的危險在于,,特朗普對傳統(tǒng)移民和對外貿(mào)易的遏制舉措可能會迫使經(jīng)濟(jì)進(jìn)入衰退期,而且情況有可能會更糟,,因為經(jīng)濟(jì)衰退會促使投資者要求美國對已然觸目驚心的債務(wù)支付更多的利息,。 說得更直白些,聯(lián)邦預(yù)算委員會稱,,即便GDP增速能夠達(dá)到特朗普團(tuán)隊所追求的3%的目標(biāo)值,,那么2028年之前所得到的額外收益也只能減少10%的總債務(wù),也就是3萬億美元,??铺卣f:“經(jīng)濟(jì)增速增加1%對于解決赤字問題也只是杯水車薪?!睘榱舜_保經(jīng)濟(jì)的長期穩(wěn)定發(fā)展,,決策者將不得不執(zhí)行在近期看來不可思議的舉措,,即同時削減開支并提升財政收入。 最近的財政立法讓開支和收入發(fā)生了負(fù)面的結(jié)構(gòu)性變化,,也會讓控制債務(wù)的任務(wù)比哪怕一年前都更難以執(zhí)行,。 在特朗普推行稅收削減之前,國會預(yù)算委員會曾預(yù)測聯(lián)邦稅收會出現(xiàn)穩(wěn)健增長,,從占GDP的17.7%到10年后的約18.4%,。然而,由于稅收削減的出現(xiàn),,2018年財政收入預(yù)計僅占GDP的17.2%,。政府開支則必然會從2018年占GDP的20.5%升至2027年的23.6%(國會預(yù)算委員會并未預(yù)測這一日期之后的數(shù)據(jù))。但2月的預(yù)算方案將引發(fā)可自由支配開支從2019年開始大幅下降,,導(dǎo)致2027年開支占GDP的整體比重升至24.8%,。 財政改革的一個重要政策便是減緩在福利保障方面的失控開支,也就是社保和醫(yī)療,。簡單來說,,美國令人生畏的人口結(jié)構(gòu)注定了福利計劃會繼續(xù)占用越來越多的財政收入。美國人口中65歲以上人群數(shù)量的增速大大高于勞動力的增速,。2017年到2030年,,超過2000萬嬰兒潮年代出生的人群將步入退休年齡,而僅有1400萬美國人會加入就業(yè)群體,。醫(yī)療所覆蓋的老年群體也在變老,,其患病的幾率也就更高。大量的高齡美國民眾會通過選票來保護(hù)其享有的福利,。 然而,,我們可以采取一些辦法來降低福利保障開支的增長。在社保方面,,針對未來10年中退休人員預(yù)計獲得的每1.10美元福利,,納稅人應(yīng)向其信托基金中投放1美元。將福利與通脹掛鉤而不是與薪酬掛鉤,,后者的年增速預(yù)計將超出前者1.5個百分點,,此舉將讓福利計劃重回平衡,同時不會破壞購買力,。在醫(yī)保方面,,政府可通過獲得處方藥議價權(quán)以及重新要求制藥商返利來控制成本,后者會為醫(yī)療補(bǔ)助計劃帶來節(jié)省,,但不適用于醫(yī)保,。國會還可以將醫(yī)生的門診費拉低至醫(yī)生的辦公室坐診費。更加激進(jìn)的舉措包括引入市場機(jī)制,,讓病患成為對成本敏感的消費者,。還有一條建議:為老年人發(fā)放固定額度的資金,,以購買私人保險。 進(jìn)一步放緩軍費和其他可自由支配開支的增幅并不是件容易事,,但過去也曾實現(xiàn)過,。國會應(yīng)按照預(yù)算控制法案,設(shè)立新的開支上限,。該法案曾在2013-2017年期間幫助減少了開支占國家財政收入的比重,。然而,由于我們觀望的時間過長,,即便推行重大的開支改革,,這個深坑依然存在,只能靠稅收來填補(bǔ),。 在拿出解決方案之前觀望的時間越長,,所需征收的新稅率也就會越高?!敦敻弧吩鴮γ绹谖磥?0年之內(nèi)所需獲取的額外財政收入進(jìn)行過計算,,條件包括社保增速降低1個百分點,大幅減少醫(yī)保,、醫(yī)療補(bǔ)助和其他醫(yī)療開支,,并讓可自由支配開支的增幅低于GDP(雖然得從新法所確立的更高的基準(zhǔn)開始)。為了方便計算,,我們假設(shè)現(xiàn)任政府不會調(diào)高企業(yè)稅,。我們的目標(biāo)是讓債務(wù)占GDP比重能夠保持在或低于2017年年底76%的水平,從而得出所需的開支削減和財政收入增幅,。盡管這一比例大約是過去50年平均值的兩倍,,但按照國會預(yù)算委員會對于未來的低利率環(huán)境預(yù)測,這個比例還是可承受的,。 正常的成本如下,。如果我們現(xiàn)在開始改革,包括開支的削減,,美國政府需要在2018年底-2028年期間每年獲得9000億美元的企業(yè)稅增量,也就是將這一期間的聯(lián)邦稅率調(diào)高21%-22%,。(如果近期赤字增加立法未能推行,,而且我們在眼下就進(jìn)行改革,所需的稅率增幅還不到這一數(shù)字的一半,。)如果我們再等上4年,,然后在2023年開始計算未來10年的狀況。我們將不得不應(yīng)對這4年期間債務(wù)的大幅增長,。如果要讓債務(wù)占GDP的比重在2032年依然維持在76%的水平,,以當(dāng)前稅收為基準(zhǔn)線,,美國的年均稅收增量應(yīng)達(dá)到1.2萬億美元,也就是24%的稅率增幅,。 一名經(jīng)濟(jì)師指出,,如果國會希望解決債務(wù)危機(jī),“無論他們采取何種舉措,,這些舉措在現(xiàn)在看來都是不可能推行的,。” 什么樣的稅可以帶來如此可觀的財政收入,。里根政府期間國會預(yù)算委員會主任魯?shù)婪颉づ謇照f:“美國政府可謂是最大程度地利用了個人所得稅這顆搖錢樹,。”他如今擔(dān)任城市研究所研究員,。曼哈頓研究所的瑞德爾認(rèn)為,,將最高的兩檔個人所得稅稅率調(diào)至70%和74%(從政治上來講是不可能的事)也只能填補(bǔ)30年中醫(yī)保和社保所缺資金的五分之一。其他的建議包括對汽油銷售征收碳排放稅,,通過向企業(yè)強(qiáng)制推行如今適用于個人的相同稅收抵扣上限來限制企業(yè)的州稅抵扣,,以及對雇主提供的高額醫(yī)療保險計劃征稅。 然而,,如果依靠現(xiàn)有的稅法,,這個數(shù)字是無法企及的?;旧厦恳粋€工業(yè)化國家都已采用消費稅來補(bǔ)貼其福利系統(tǒng),。平均來看,增值稅占到了這些稅收的約60%,,它與銷售稅類似,,發(fā)生在商品經(jīng)歷的每個生產(chǎn)環(huán)節(jié),實際上由公司來支付,。這類稅收平均貢獻(xiàn)了約6%的GDP,,其通常的稅率約為20%。 美國沒有增值稅或全國性的銷售稅,,但由于此類稅種在其他國家會蠶食掉很大一部分的收入,,因此我們也就不難理解為什么這一稅種會在國會遇冷。然而,,由于我們的財政即將陷入絕境,,美國可能很快就會發(fā)現(xiàn),政府需要采取一些以前從未考慮過的解決方案,。帶有自由主義傾向的布魯金斯研究所的經(jīng)濟(jì)師威廉·蓋爾說:“特朗普政府和這屆國會不會考慮推出增值稅,,但其呼聲將高漲。無論最終采取何種舉措,這些舉措在現(xiàn)在看來都是不可能推行的,?!薄? 確實,,如果美國政客們最終都下定了決心,,并盡其所能為美國財政尋找一個堅實的落腳點,那么他們必然會經(jīng)歷難以想象的痛苦,。即便可以采用調(diào)高稅率的辦法,,他們?nèi)孕枰獜囊粋€高起點出發(fā),因為我們等待的時間已經(jīng)太久了,,他們將以這一起點為基礎(chǔ)來調(diào)高稅率,。美國此前從未經(jīng)歷過這種幅度的增稅,但這是很有可能發(fā)生的,。不久之后,,消費者可用于汽車、電器,、iPhone和度假方面的資金將減少,。公司的銷售和盈利也將因此而受到?jīng)_擊。同時,,這一可能發(fā)生的消費陣痛或許會給政客們帶來壓力,,迫使他們至少撤銷某些特朗普尤為引以自豪的公司稅削減政策。 大衛(wèi)·科特回憶道,,他在一開始加入辛普森-鮑勒斯委員會時曾力推增值稅,。“然后,,有些人指出,,美國政府不需要制造一個新的稅收引擎,后來我轉(zhuǎn)而反對增值稅,,因為它只會繼續(xù)推高支出,。”但不管怎么樣,,政府支出一直在不斷增加,,如今,支出增幅更是得到了共和黨立法主體和這位民粹總統(tǒng)的支持,。在預(yù)算事務(wù)方面,,美國民眾熱衷于高福利的銳不可當(dāng)之勢與美國民眾拒絕高稅收的無法撼動之心發(fā)生了沖突。就像強(qiáng)尼·莫瑟的那首老歌所唱的那樣——“總得付出點代價”,。(財富中文網(wǎng)) 本文的一個版本刊登于《財富》2018年4月刊,標(biāo)題為《深陷債務(wù)泥潭》,。 譯者:Ms? |

As business-friendly as Trump’s tax and regulation stances may be in the short term, these policies are growth killers. The overriding danger is that by pushing hard against traditional immigration and open trade, Trump could force the economy into a recession—one that could be made worse because it would prompt investors to ask for higher interest on our already gigantic debt. Perhaps more to the point: Even if GDP did wax at the 3% level that the Trump team seeks, the extra juice would lower total debt by only 10%, or $3 trillion, by 2028, according to the CRFB. “Adding a point to growth won’t come close to solving the problem,” says Cote. To ensure long-term stability, policymakers will have to do something that’s been almost unthinkable in recent memory—simultaneously cut spending and pump up revenue. The recent fiscal legislation caused negative, structural changes on both the spending and revenue fronts—making the task of keeping the debt in check much harder than it would have been even a year ago. Prior to the Trump tax cuts, the CBO was projecting that federal tax revenues would grow robustly, from 17.7% of GDP in 2018 to around 18.4% a decade later. But because of the cuts, revenues in 2018 are projected to be just 17.2% of national income. Government spending, meanwhile, was set to expand from 20.5% of GDP in 2018 to 23.6% in 2027 (the CBO did not project the figure after that date). But the February deal will trigger a huge jump in discretionary spending starting in 2019, raising the overall 2027 figure to 24.8% of GDP. A crucial plank in fiscal reform is slowing runaway spending on entitlements, chiefly Social Security and Medicare. Put simply, the nation’s daunting demographic math dictates that the benefit programs keep absorbing bigger and bigger shares of national income. The cohort of Americans over age 65 is expanding much faster than the workforce; from 2017 to 2030, 20 million more baby boomers will reach retirement age, while only 14 million Americans will begin employment. The pool of seniors on Medicare is also getting older, and as a result, sicker. And older Americans vote, in huge numbers, to protect their privileges. Still, there are ways to slow entitlement growth. In Social Security, taxpayers will contribute about $1 to its trust fund for every $1.10 retirees are projected receive in benefits over the next decade. Indexing benefits to inflation instead of wages, the latter of which are forecast to grow 1.5 percentage points faster annually, would return the program to balance without damaging purchasing power. On Medicare, the government could restrain costs by gaining authority to negotiate prices for prescription drugs, and by reinstating the requirement that drugmakers provide rebates, a policy that generates savings for Medicaid but is barred for Medicare. Congress could also set doctors’ fees for outpatient hospital visits to the lower rates charged for office consultations. Bolder moves include introducing market forces that turn patients into cost-conscious consumers. One prescription: Giving seniors fixed payments to buy private insurance. Getting military and other discretionary spending to grow less slowly won’t be easy, but it has been done in the past. Congress should enact new spending caps along the lines of the Budget Control Act, which helped to shrink outlays as a share of national income from 2013 to 2017. But because we’ve waited so long, even major spending reforms leave a big hole—a chasm that can be filled only by taxes. The longer we wait to enact a solution, the higher the new levies required will need to go. Fortune ran numbers to calculate how much extra revenue the U.S. would need to raise, over the next decade, if it lowered the rate of growth in Social Security by one percentage point, reduced increases in Medicare, Medicaid, and other health care spending by a proportional amount, and held discretionary spending below growth in GDP (albeit from the higher base established by the new laws). For our purposes, we assumed that corporate tax increases are off the table under the current administration. Our goal was to come up with spending cuts and revenue increases that would keep the ratio of debt to GDP at or below where it was at the end of 2017, at 76%. Though that’s around twice the average over the past 50 years, it’s what would be affordable given the CBO’s projections of low interest rates for years to come. So here’s what the cost of sanity looks like. If we start reforms now, including the slowdown in spending, the government would need to phase in noncorporate tax increases averaging $900 billion a year from the end of 2018 through 2028. That would require raising federal tax collections by between 21% and 22% over that period. (That’s more than twice the increase we would have needed if we’d started now, without the recent deficit-ballooning legislation.) What if we wait four years, and begin our 10-year projections at the start of 2023? We’d be coping with four more years of colossal growth in debt. To wrestle the debt-to-GDP ratio back to 76% by 2032, the U.S. would require an average tax increase of $1.2 trillion over today’s baseline. That’s a rise of 24%. If congress hopes to solve the debt crisis, says one economist, “whatever they come up with will be something that seems impossible now.” What kind of taxes could produce that bounty? “We’ve gotten about as much money as we can out of the personal income tax,” says Rudolph Penner, director of the CBO during the Reagan administration and now a fellow at the Urban Institute. Riedl, of the Manhattan Institute, reckons that doubling the top two personal rates to 70% and 74% respectively (politically a near-impossibility) would close just one-fifth of the projected shortfall from Medicare and Social Security over 30 years. Other proposals include a carbon tax on gasoline sales, limiting deductibility of state taxes for businesses by imposing the same caps that now apply to individuals, and taxing generous employer-provided health care plans. But it’s unlikely that anything close to the necessary number can be raised by tinkering with the existing tax code. Virtually every other industrialized country deploys consumption taxes to support their welfare states. On average, around 60% of those levies are value-added taxes, or VATs, which resemble a sales tax but are actually paid by companies as goods go through each stage of production. They raise, on average, about 6% of GDP, at typical rates of roughly 20%. The U.S. doesn’t have a VAT or a national sales tax—and given how enormous a bite such taxes take out of income in other countries, it’s easy to see why they haven’t gained traction in Congress. But our fiscal plight is becoming so desperate that America may soon find itself embracing solutions it never before contemplated. “A VAT won’t happen under this President and this Congress, but its stock will rise,” says William Gale, an economist at the liberal-leaning Brookings Institution. “Whatever they come up with will seem to be something that’s impossible now.” Indeed, if our politicians finally grow a collective backbone and strive to put America’s finances on a firm footing, the pain will be wrenching. Even though tax increases can be phased in, they’ll still need to start at a high plateau because we’ve waited so long, and they’ll rise from there. America has never seen anything like the kind of tax hikes that could be in the cards. Over time, consumers will have less to spend on cars, appliances, iPhones, and vacations. Sales and profits will suffer. And the likely consumer pain might generate political pressure to undo at least some of the corporate tax cuts that Trump is so proud of. Dave Cote recalls that he favored a VAT when he first joined the Simpson-Bowles Commission. “Then someone pointed out that the government doesn’t need a new engine to collect taxes, and I changed to opposing the VAT because it would just keep ratcheting up spending.” But government spending has ratcheted up anyway—now with the blessing of the Republican legislative majority and a populist President. On budget matters, the irresistible force of Americans’ love for rich benefits collides with the immovable object of Americans’ resistance to high taxes. As the old Johnny Mercer song goes, “Something’s Gotta Give.” A version of this article appears in the April 2018 issue of Fortune with the headline “Deep in Debt.” |