這位傳奇投資人在這兩家傳奇企業(yè)的身上栽了跟頭

|

今年10月1日,,通用電氣宣布解雇僅就職14個(gè)月的首席執(zhí)行官約翰·弗蘭納里,鮮少有人不對(duì)此感到震驚,,但大名鼎鼎的激進(jìn)投資者納爾遜·佩爾茨就是其中之一,。甚至連一直執(zhí)著于跟蹤這家風(fēng)光不再的企業(yè)動(dòng)態(tài)的華爾街分析師都因?yàn)楦ヌm納里的突然被炒而感到驚訝。然而佩爾茨對(duì)此并非事先不知情,,因?yàn)樗谔乩锇矊?duì)沖基金的合伙人愛(ài)德華·加登是通用電氣的董事會(huì)成員,,正是董事會(huì)炒了弗蘭納里。特里安擁有7100萬(wàn)股通用電氣股票,,通用電氣也因而成為佩爾茨多年來(lái)十分成功的職業(yè)生涯中損失最慘重的投資,。由于該公司最近披露的負(fù)債據(jù)說(shuō)受到了聯(lián)邦刑事調(diào)查,公司股票再度下跌,,佩爾茨持有的股票和三年前買(mǎi)入時(shí)相比,,已經(jīng)虧損逾10億美元,跌幅達(dá)約50%,。隨著弗蘭納里迅速遭到無(wú)情拋棄,,佩爾茨明白變化正在醞釀中。 佩爾茨比大多數(shù)人都更能適應(yīng)巨變,。所謂激進(jìn)投資人指的是不滿(mǎn)足于袖手旁觀(guān)的投資人,,而在這類(lèi)投資者中,佩爾茨在推動(dòng)變化方面也是佼佼者,。作為激進(jìn)派投資者,,他曾對(duì)多家公司發(fā)起過(guò)突襲,包括推動(dòng)杜邦在與陶氏化學(xué)合并后再分拆為三家獨(dú)立公司,。他還促使卡夫分為卡夫食品集團(tuán)和億滋國(guó)際,。他試圖拆分百事可樂(lè),但失敗了。這是一位野心勃勃的投資人,。 但在他諸多野心勃勃的計(jì)劃中,,對(duì)通用電氣和位于其待辦事項(xiàng)清單頂端的另一家公司寶潔的野心可謂最大。寶潔沒(méi)有失敗,,因?yàn)樽耘鍫柎耐顿Y以來(lái),,該公司的股價(jià)小幅上漲,而且它顯然比通用電氣更有希望,。11月,,寶潔宣布了重組計(jì)劃,,雖然是在佩爾茨一直力推的計(jì)劃上打了折扣,。一年前佩爾茨和寶潔打了美國(guó)歷史上最昂貴的代理權(quán)爭(zhēng)奪戰(zhàn),并最終在3月加入公司董事會(huì),,但該公司遠(yuǎn)未取得佩爾茨所希冀的成功,。寶潔的股價(jià)上漲緩慢,佩爾茨的股權(quán)目前價(jià)值35億美元,,是價(jià)值100億美元的特里安目前的最大投資,。因此佩爾茨要想依靠寶潔擺脫通用電氣崩潰帶來(lái)的困境,寶潔的表現(xiàn)要有顯著好轉(zhuǎn)才行,。(因?yàn)榕鍫柎氖菍殱嵉亩?,而他的女婿加登是通用電氣的董事,他們拒絕了本文的采訪(fǎng)請(qǐng)求,。) 通用電氣和寶潔一同毀掉了特里安此前優(yōu)秀的投資記錄:過(guò)去五年,,特里安的收益率高達(dá)年均11.9%,成績(jī)不俗,;過(guò)去三年,,是平淡無(wú)奇的年均6.5%;據(jù)特里安的一名投資者稱(chēng),,截至10月,,2018年的數(shù)字大約是令人沮喪的-1%。佩爾茨的大部分個(gè)人財(cái)富和高績(jī)效激進(jìn)投資人的美譽(yù)都綁在了這兩家公司身上,。 佩爾茨在通用電氣和寶潔公司能干成什么樣非常重要,,因?yàn)檫@兩家知名公司不但都是佩爾茨的大難題,還擁有許多共同點(diǎn),。這兩家美國(guó)公司在世界各地都被譽(yù)為公司中的貴族,,擁有100多年的血脈延續(xù)。兩家公司又都擁有各自獨(dú)特又不容改變的企業(yè)文化,,而且這些文化都形成于公司在市場(chǎng)上獨(dú)領(lǐng)風(fēng)騷的時(shí)期,。但它們又都已經(jīng)風(fēng)光不再。依靠在兩家公司的董事會(huì)席位,特里安正不斷嘗試突破它們的界限,,試圖實(shí)現(xiàn)更大目標(biāo),。除了利用分拆、削減成本,、借貸等激進(jìn)投資者常用的工具,,特里安和其他激進(jìn)投資人相比,更愿意深入鉆研公司運(yùn)營(yíng),,有時(shí)他們會(huì)花費(fèi)數(shù)年時(shí)間幫助公司管理層解決經(jīng)營(yíng)問(wèn)題,。由于采取顛覆性措施對(duì)老牌大公司產(chǎn)生更大的威脅,所以特里安能否在通用電氣和寶潔實(shí)現(xiàn)成功可以幫助我們判斷,,如果激進(jìn)投資人或任何局外人想要改變?cè)?jīng)統(tǒng)治世界的公司,,在這種最高難度的經(jīng)營(yíng)難題中他們可以取得多少成績(jī)。 |

On Oct. 1, when General Electric announced it had fired John Flannery, its CEO of just 14 months, one of the few people not at all shocked by the news was Nelson Peltz, the legendary activist investor. Flannery’s abrupt dismissal surprised even Wall Street analysts who obsessively follow the tarnished conglomerate. Yet Peltz wasn’t caught off guard, because his partner at the Trian hedge fund, Edward Garden, is on the GE board of directors that did the deed. Trian owns 71 million shares of GE stock, qualifying GE as Peltz’s most disastrous investment in a long, successful career. He’s down over $1 billion, about 50%, since buying in three years ago, with the stock’s latest drop following word of a federal criminal investigation into recently disclosed liabilities. With the brutally swift cashiering of Flannery, Peltz now understood change was afoot. More than most, Peltz is comfortable with dramatic change. No other activist, a class of investors not content merely to watch from the sidelines, has prompted more of it. Among many activist forays, he instigated the transformation of DuPont into three independent companies after first combining with Dow Chemical. He forced the separation of Kraft into Kraft Foods Group and Mondelez International. He tried and failed to break up PepsiCo. He thinks big. He has never thought bigger than he did with GE and with the other company at the top of his to-do list, Procter & Gamble. P&G is no disaster—its shares are up slightly since Peltz invested—and it’s decidedly more promising than GE. In November, the company announced a watered-down version of the reorganization plan he had been pushing. But the company is nowhere near the success Peltz wants it to be, a year after he battled P&G in the most expensive proxy fight in U.S. history and gained a board seat in March. P&G stock is a laggard, and Peltz’s stake, recently worth $3.5 billion, is by far the biggest investment in $10 billion Trian. So Peltz needs it to perform much better if it’s to help rescue him from the GE debacle. (Because Peltz is on the P&G board, and Garden, his son-in-law, is on the GE board, they declined interview requests for this article.) Together, GE and P&G have mauled Trian’s previously sterling record: Over the past five years, Trian’s rate of return has averaged an outstanding 11.9% annually; over the past three years, a mediocre 6.5% annually; in 2018 through October, a dismal –1% or so, according to a Trian investor. Much of Peltz’s personal wealth and his reputation as a high-performing activist are tied up in those two companies. How Peltz fares with GE and P&G is important because the two famed companies share many traits besides being Peltz’s biggest problems. They’re American institutions, storied worldwide as corporate aristocrats with bloodlines stretching back more than a century. Each lives according to a unique, titanium-strength corporate culture that developed back when they were supremely dominant. Neither company has retained its stature, though. With board seats at both, Trian is pressing the boundaries of what can be accomplished at such organizations. In addition to bringing the activist’s usual tools—breakups, cost cutting, borrowing—the firm is willing to delve more deeply into operations than any other activist and sometimes spends years helping management fix a business. As disruption threatens more big, old incumbents, Trian’s success or failure will help define how much an activist, or any outsider, can hope to achieve in that hardest of managerial challenges, transforming a company that once ruled the world. |

|

佩爾茨不是一般的激進(jìn)投資人,,特里安也不是一般的對(duì)沖基金,通用電氣也不是特里安的一般投資?,F(xiàn)年76歲的佩爾茨將他的激進(jìn)投資歷史追溯至20世紀(jì)80年代中期邁克爾·米爾肯以及他資助的一票企業(yè)狙擊手的鼎盛時(shí)期,。 除了佩爾茨,還包括卡爾·伊坎,、索爾·斯坦貝克,、T·布恩·皮肯斯等。與當(dāng)時(shí)的許多人不同,,佩爾茨對(duì)所謂的綠票訛詐不感興趣,,這種戰(zhàn)術(shù)指的是大量購(gòu)買(mǎi)公司股票,威脅管理層要收購(gòu)公司,、迫其失業(yè),,表示如果公司高價(jià)回購(gòu)綠票訛詐者所持股票就會(huì)離場(chǎng)。佩爾茨看到了能賺更多錢(qián)的機(jī)會(huì),。 他覺(jué)得自己能成功,,因?yàn)椴煌?0世紀(jì)80年代的其他狙擊手,也不同于今天的激進(jìn)投資人,,他曾經(jīng)在遠(yuǎn)離華爾街的地方做過(guò)生意,。他和他的兄弟將家里的食品分銷(xiāo)業(yè)務(wù)做成了一家名為弗拉格斯塔夫(Flagstaff)的冷凍食品公司;直到今天,,特里安仍然熱衷于食品企業(yè),,并投資了多家食品公司,如Wendy’s、卡夫,、亨氏,、百事可樂(lè)等等。佩爾茨40歲時(shí),,弗拉格斯塔夫公司破產(chǎn)了,,但他顯然從中學(xué)到了教訓(xùn)。他和曾擔(dān)任弗拉格斯塔夫首席財(cái)務(wù)官的會(huì)計(jì)師彼得·梅收購(gòu)了Triangle Industries,,這家自動(dòng)售貨機(jī)和電線(xiàn)公司被他們打造成了全球《財(cái)富》100強(qiáng)工業(yè)集團(tuán),,后來(lái)在1988年被賣(mài)出。從那之后,,佩爾茨和梅就一直在從事收購(gòu)公司,、進(jìn)行業(yè)務(wù)修復(fù)再賣(mài)出公司的營(yíng)生。2005年,,他們和第三個(gè)合伙人,、曾任瑞士信貸第一波士頓公司(Credit Suisse First Boston)投資銀行家的加登共同創(chuàng)立了特里安,。據(jù)特里安表示,,曾在佩爾茨和杜邦及寶潔的代理人之爭(zhēng)中為其提供支持的加州教師退休基金(State Teachers’ Retirement System)及其他機(jī)構(gòu)投資者占公司全部資產(chǎn)的75%。 “采取修復(fù)措施,,讓公司經(jīng)營(yíng)好轉(zhuǎn)——這就是我們的工作,。”57歲的加登在3月的一次投資會(huì)議上說(shuō),?!拔覀儗ふ业墓驹诒举|(zhì)上都是偉大的公司,雖然管理層在運(yùn)營(yíng)方面偏離軌道,,但我們相信自己知道如何讓他們的業(yè)務(wù)重回正軌,。”如果你覺(jué)得這聽(tīng)起來(lái)更像是私募股權(quán),,特里安也同意這種看法,。“我們認(rèn)為自己是一種新的資產(chǎn)類(lèi)別,,”他說(shuō),。“可以稱(chēng)為‘流動(dòng)型私募股權(quán)’或‘混合型私募股權(quán)’,?!碧乩锇驳哪繕?biāo)是獲得和私募股權(quán)同等規(guī)模的回報(bào),但不必像私募公司那樣買(mǎi)下整個(gè)公司或大額股份,。特里安僅擁有寶潔公司1.5%的股份和通用電氣公司0.8%的股份,。通過(guò)改善目標(biāo)公司運(yùn)營(yíng),長(zhǎng)期持有目標(biāo)公司股權(quán),特里安即使不使用杠桿,,也能夠獲得更高收益,,比僅僅依靠交易賺取更高的績(jī)效費(fèi)。 2015年春天,,特里安成功結(jié)束了四項(xiàng)投資——達(dá)能,、家庭美元百貨(Family Dollar)、英格索蘭(Ingersoll-Rand)和拉扎德(Lazard),,準(zhǔn)備開(kāi)展其它投資項(xiàng)目,。通用電氣公司顯然符合特里安的投資標(biāo)準(zhǔn)——一家脫離了軌道的偉大公司,而且碰巧,,時(shí)任通用電氣公司首席執(zhí)行官的杰夫·伊梅爾特邀請(qǐng)佩爾茨買(mǎi)進(jìn)公司股份,。兩年前,伊梅爾特甚至安排佩爾茨向公司頂級(jí)管理人員講授如何削減成本,。這種開(kāi)放的歡迎態(tài)度幾乎聞所未聞:通常情況下,,特里安的目標(biāo)公司會(huì)試圖擊退入侵者,至少在最初階段會(huì)是如此,。巨大的老牌工業(yè)公司不是佩爾茨的專(zhuān)長(zhǎng),,但重點(diǎn)是伊梅爾特向華爾街承諾,通用電氣將在2018年實(shí)現(xiàn)每股盈利2美元,,而2015年的持續(xù)性經(jīng)營(yíng)每股收益僅為17美分,。特里安認(rèn)為通用電氣甚至能表現(xiàn)更好,能實(shí)現(xiàn)2.20美元或以上的盈利,;當(dāng)時(shí)26美元的股價(jià)在2017年年底應(yīng)該達(dá)到40到45美元之間,。佩爾茨購(gòu)買(mǎi)了23億美元的通用電氣股票并告訴伊梅爾特,特里安將確保他能夠?qū)崿F(xiàn)每股2美元收益的承諾,。 當(dāng)年秋天,,特里安發(fā)布了通用電氣“白皮書(shū)”,這份81頁(yè)的PPT對(duì)通用電氣的戰(zhàn)略和股票都提出了有力支持,。的確,,公司需要降低成本、削減管理層,,而且可以增加借貸,。但本質(zhì)上,這不過(guò)是伊梅爾特“大幅改變其商業(yè)模式”的一個(gè)例子——大幅剝離GE金融業(yè)務(wù),,從公司的服務(wù)業(yè)務(wù)而非銷(xiāo)售中獲得收入——特里安認(rèn)為這“在市場(chǎng)上未得到充分重視”,。之后股價(jià)上漲,佩爾茨賣(mài)出了一些,,撤出了近4億美元的資金,,事后回想這實(shí)在是明智之舉,。公司股票繼續(xù)上漲,達(dá)到金融危機(jī)前未曾企及的高度,,于2016年12月沖上32.38美元,。 讓人頭疼的擔(dān)憂(yōu)首先出現(xiàn)在2016年第四季度。通用電氣的轉(zhuǎn)型十分昂貴:該公司支付的現(xiàn)金超過(guò)了收入,,其養(yǎng)老基金短缺310億美元,。僅2015年支付的股息就高達(dá)93億美元,比通用電氣的全部?jī)衄F(xiàn)金流都要多,。此外,,通用電氣最大的業(yè)務(wù)是為電力企業(yè)提供巨型渦輪機(jī),相關(guān)訂單量卻未達(dá)預(yù)期,。不過(guò),,這種和期望值之間的差距可以說(shuō)成是可逆的,投資者似乎并不擔(dān)心,。 如果當(dāng)時(shí)佩爾茨對(duì)通用電氣感到擔(dān)心的話(huà),,他似乎不太可能在那個(gè)時(shí)刻對(duì)另外一個(gè)陷入麻煩的巨人再下高額賭注。就在幾個(gè)星期前,,隨著他的通用電氣股價(jià)升值,,佩爾茨買(mǎi)入了首批寶潔股票。截至2017年年初,,這是特里安新近投資中最大的一筆,,價(jià)值33億美元,。盡管寶潔不再?gòu)氖屡鍫柎淖钕矚g的食品生意,,卻仍然是他的理想目標(biāo)——一家偉大卻架構(gòu)過(guò)于復(fù)雜、需要整頓的公司,。寶潔旗下包括吉列剃須刀,、佳潔士牙膏、潘婷洗發(fā)水在內(nèi)的數(shù)十個(gè)最知名品牌正在失去市場(chǎng)份額,;全部五個(gè)產(chǎn)品類(lèi)別都失去了競(jìng)爭(zhēng)優(yōu)勢(shì),。公司的其他投資者很高興看到佩爾茨出手,這只在牛市都停滯多年的股票在佩爾茨入場(chǎng)后一度飆升,。 華爾街喜迎佩爾茨,,但寶潔公司的領(lǐng)導(dǎo)層卻并不歡迎他的加入。該公司發(fā)布聲明,,感謝全體股東,,但管理層想到未來(lái)要由外人對(duì)他們指手畫(huà)腳便感到深?lèi)和唇^。佩爾茨與首席執(zhí)行官戴維·泰勒以及董事會(huì)的會(huì)議令雙方都備感沮喪,。2017年6月,,有消息說(shuō)佩爾茨提名自己擔(dān)任公司董事時(shí),,投資者一片歡呼,股票再次大漲,。但頗為諷刺的是,,寶潔公司的領(lǐng)導(dǎo)層日后卻把當(dāng)時(shí)股票行情的好轉(zhuǎn)當(dāng)成證據(jù),證明不需要佩爾茨的幫助他們的戰(zhàn)略也行之有效,。 佩爾茨的請(qǐng)求遭到了寶潔的拒絕,,所以他在7月宣布開(kāi)啟代理權(quán)爭(zhēng)奪戰(zhàn)。事實(shí)證明,,這種斗爭(zhēng)費(fèi)時(shí)費(fèi)錢(qián),,令各方都感到不快。泰勒警告道,,佩爾茨分散了管理層的注意力,,會(huì)“拖累管理層正在領(lǐng)導(dǎo)公司進(jìn)行的轉(zhuǎn)型?!迸鍫柎囊辉俟_(kāi)點(diǎn)名攻擊泰勒,,并邀請(qǐng)前寶潔公司首席財(cái)務(wù)官克萊頓·戴利加入其陣營(yíng)討伐戴利的前雇主。雙方在這場(chǎng)戰(zhàn)斗中花費(fèi)巨大,,高達(dá)1億美元,,最終,寶潔在兩個(gè)月的股東投票中以50.01%比49.99%險(xiǎn)勝,,但二者的差距小到幾乎可以忽略,。董事們意識(shí)到他們的勝利實(shí)在太過(guò)微弱,沒(méi)有足夠立場(chǎng)拒絕佩爾茨的請(qǐng)求,,因此他在今年3月加入了寶潔董事會(huì),。 很難相信佩爾茨和加登在史上最大的代理權(quán)爭(zhēng)奪戰(zhàn)之外還可以關(guān)注其它事情,但他們必須得關(guān)注,。正在2017年中他們和寶潔的關(guān)系惡化時(shí),,通用電氣垮掉了。 投資者們迅速失去信心,,2018年每股2美元的盈利承諾顯然無(wú)法實(shí)現(xiàn)了,。(今天華爾街預(yù)計(jì)通用電氣的每股收益為68美分。)通用電氣投資者和分析師還能記起他們意識(shí)到伊梅爾特已經(jīng)完蛋了的那一刻,。那是2017年5月,,長(zhǎng)期擔(dān)任公司首席執(zhí)行官的伊梅爾特在佛羅里達(dá)州舉辦的年度集會(huì)上發(fā)表了講話(huà),該集會(huì)旨在為大型電子產(chǎn)品公司的首席執(zhí)行官與金融界進(jìn)行交流提供平臺(tái),?!拔覐膩?lái)沒(méi)有見(jiàn)過(guò)那樣的場(chǎng)景,”有人說(shuō),?!八呀?jīng)絕望了,。你無(wú)法忍受直視他的眼睛。最簡(jiǎn)單的基本問(wèn)題就能把他生生吃掉,?!?僅19天后,伊梅爾特宣布退休,,讓所有人都大吃一驚,。公司股票當(dāng)天用20個(gè)月內(nèi)的最佳表現(xiàn)對(duì)該新聞做出了回應(yīng)。 |

Peltz isn’t a usual activist, Trian isn’t a usual hedge fund, and GE isn’t a usual investment for it. At age 76, Peltz traces his activist roots to the mid-’80s heyday of Michael Milken and the band of corporate raiders he financed. Besides Peltz, they included Carl Icahn, Saul Steinberg, T. Boone Pickens, and others. Unlike many back then, Peltz wasn’t interested in greenmail, the strategy of buying a stake, threatening management with a takeover that would cost them their jobs, and offering to go away if the company bought back the greenmailer’s stock at a higher price. Instead, he saw a chance to make even more. He felt he could do it because, unlike virtually all the other 1980s raiders and today’s activists, he had run businesses far from Wall Street. He and his brother built the family’s food distribution business into an institutional frozen food company called Flagstaff; to this day, Trian likes food companies and has invested in many—Wendy’s, Kraft, Heinz, PepsiCo, and more. Flagstaff went bankrupt when Peltz was 40, but he apparently learned from the experience. He and Peter May, an accountant who had been Flagstaff’s chief financial officer, bought Triangle Industries, a vending machine and wire company that they built into a Fortune 100 industrial conglomerate, which they sold in 1988. He and May have been buying, fixing, and selling companies ever since. In 2005, they formed Trian with a third partner, Garden, a former Credit Suisse First Boston investment banker. Institutional investors like the California State Teachers’ Retirement System, which has backed Peltz in his proxy fights at DuPont and P&G, account for about 75% of Trian’s assets, the firm says. “Fix companies and turn businesses around—that’s what we do,” Garden, 57, told an investment conference in March. “We look for fundamentally great companies where management has gone off track operationally and where we think we understand what it takes to get the business back on track.” If that sounds to you more like private equity, Trian agrees. “We think of ourselves as a new asset class,” he said. “?‘Liquid private equity’ or ‘hybrid private equity.’?” The objective is to earn PE-scale returns without having to buy a whole company or a significant stake, as PE firms typically do; Trian owns only 1.5% of P&G and 0.8% of GE. By improving operations and holding positions for years, even without leverage, Trian hopes to generate higher returns and earn bigger performance fees than it could through trading alone. In the spring of 2015, Trian was successfully exiting four investments—Danone, Family Dollar, Ingersoll-Rand, and Lazard—and was ready to invest elsewhere. General Electric certainly met the spec of a great company that had gone off track, and as it happened, GE chief Jeff Immelt had invited Peltz to buy in. Two years earlier, Immelt had even arranged for Peltz to address his top managers on the subject of cost cutting. Such an embrace was almost unheard of; Trian’s targets usually try to repel the invader, at least initially. Giant, old industrial companies weren’t Peltz’s specialty, but Immelt, crucially, had promised Wall Street that GE would earn $2 a share by 2018, up from 17¢ per share from continuing operations in 2015. Trian concluded GE could do even better, $2.20 or more; the $26 shares ought to be worth $40 to $45 by the end of 2017. Peltz bought $2.3 billion of GE stock and told Immelt that Trian would hold him accountable for keeping the $2-a-share promise. That fall, Trian published a “white paper” on GE, an 81-page PowerPoint deck powerfully endorsing GE’s strategy and its stock. Yes, the company needed to cut costs and excise management layers, and it could borrow more. But this was fundamentally a case of Immelt making “a massive change in its business model”—exiting most of GE Capital and targeting more revenue from services rather than from sales—that was “under-appreciated in the market,” Trian argued. The stock rose, and Peltz sold some, taking almost $400?million off the table, which in retrospect was a wise move. The stock continued drifting up, reaching heights it hadn’t achieved since before the financial crisis and touching $32.38 in December 2016. Nagging doubts first appeared in 2016’s fourth quarter. GE’s transformation was expensive; the company was paying out more cash than it was taking in, and its pension fund was underfunded by $31 billion. Dividend payments alone, at $9.3 billion in 2015, consumed more than GE’s entire free cash flow. In addition, GE’s biggest business, which makes gigantic turbines for electric utilities, wasn’t booking as many orders as anticipated. Still, the shortfall was arguably reversible, and investors didn’t seem worried. Had Peltz been worried about GE, it seems unlikely he would have picked that moment to make another massive bet on a troubled titan. Just weeks earlier, with his GE stake appreciating, Peltz bought his first tranche of Procter & Gamble stock. By early 2017, it was Trian’s new largest investment, worth $3.3 billion. P&G no longer marketed food, Peltz’s favorite business, but this was still his ideal target, a great company that had grown far too complex and needed shaking up. Dozens of its most famous brands—including Gillette razors, Crest toothpaste, and Pantene shampoo—were losing market share; all five of its product categories had lost significant ground to competitors. Other investors were glad to see Peltz; the stock, which had gone nowhere for years while the market surged, jumped on Peltz’s entry. Wall Street gladly greeted Peltz’s arrival, but P&G’s leaders did not. The company issued the obligatory statement about appreciating all its shareholders, but managers loathed the prospect of an outsider telling them how to do things. Peltz’s meetings with CEO David Taylor and the board frustrated both sides. When word leaked in June 2017 that Peltz had nominated himself for a board seat, investors cheered, and the stock jumped again. Ironically, P&G leaders would later cite the stock’s improved performance as evidence that their strategy was working fine without Peltz’s help. P&G rejected Peltz’s request, so in July he announced a proxy fight. The ordeal proved expensive, nasty, and long. Taylor warned that by distracting management, Peltz could “derail the transformation we’re leading.” Peltz repeatedly attacked Taylor by name and enlisted former P&G CFO Clayton Daley to campaign against his former employer. The two sides spent lavishly, as much as $100 million, on the battle, and in the end, P&G won a two-month shareholder vote by the nearly invisible margin of 50.01% to 49.99%. The directors realized the victory was too narrow to deny Peltz a seat, and he joined the board this past March. It’s hard to believe that Peltz and Garden could have focused on anything besides the world’s all-time biggest proxy fight, but they had to. Just as relations with P&G were deteriorating in mid-2017, GE was melting down. Investors were fast losing faith, and it was becoming apparent that the $2-a-share earnings promise for 2018 wasn’t achievable. (Today Wall Street expects GE earnings of 68¢ per share.) GE investors and analysts recall the moment they realized Immelt was through. It was the longtime CEO’s presentation at an annual May ritual in Florida where CEOs of big companies that make electrical products speak to the financial community. “I’ve never seen anything like it,” says one. “He was a broken man. You couldn’t stand to look him in the eye. He got eaten alive by basic, simple questions.” Just 19 days later, Immelt surprised everyone by announcing his retirement. The stock responded with its best day in 20 months. |

|

由于伊梅爾特的承諾徹底沒(méi)有兌現(xiàn),,特里安關(guān)于通用電氣的計(jì)劃變成了一團(tuán)糟,,加登和佩爾茨不再只是詢(xún)問(wèn)有關(guān)董事會(huì)席位的情況,而是要求在董事會(huì)中取得一席,。與此同時(shí),,佩爾茨在與寶潔的代理權(quán)爭(zhēng)奪戰(zhàn)中展示了他的兇悍。通用電氣在10月讓加登加入其董事會(huì)——不需要代理權(quán)爭(zhēng)奪戰(zhàn),。 此后,,通用電氣的情況一再惡化。該公司相應(yīng)采取的舉措中,,最引人注目的是對(duì)董事會(huì)進(jìn)行徹底重組,,加登進(jìn)入董事會(huì)后沒(méi)多久董事會(huì)就開(kāi)始了重組。18位董事中有一半離職——這是前所未有的叛變——被三位新董事取代,,其中一位是拉里·卡爾普,。這立刻引發(fā)了人們的猜測(cè):他是不是候任首席執(zhí)行官?如果是這樣,,背后是不是特里安在支持,?該公司未就此發(fā)表評(píng)論,但在去年5月發(fā)布了一份關(guān)于本公司的情況說(shuō)明書(shū),,稱(chēng)“三名新董事加入董事會(huì),,其中包括丹納赫集團(tuán)的前任首席執(zhí)行官拉里·卡爾普”,卻未提及另外兩名董事的名字,。有業(yè)內(nèi)人士表示,卡爾普否認(rèn)有出任首席執(zhí)行官的想法——顯然證明了存在這種可能性,。 從特里安的角度來(lái)看,,通用電氣董事會(huì)的改革算得上是重大進(jìn)展。佩爾茨進(jìn)入寶潔公司董事會(huì)后,,該公司也隨之取得了更多進(jìn)展,。代理權(quán)斗爭(zhēng)中的齟齬消失得無(wú)影無(wú)蹤?!拔覀冏鹬丶{爾遜·佩爾茨……并期待他以寶潔董事會(huì)成員的身份做出貢獻(xiàn),?!碧├赵谝环萋暶髦姓f(shuō)。佩爾茨說(shuō)他“期待與泰勒緊密合作”,。能看出佩爾茨正在領(lǐng)導(dǎo)變革的第一個(gè)線(xiàn)索是7月發(fā)布的一份證券文件,,該文件披露了寶潔公司已經(jīng)修改了高管的薪酬獎(jiǎng)勵(lì)計(jì)劃,更多地將薪酬與個(gè)人績(jī)效掛鉤,,而非公司業(yè)績(jī),。這是典型的佩爾茨式做法,隨后公司在11月進(jìn)行了一次更加重大的變革,,將公司重組為六個(gè)部門(mén),,賦予每個(gè)部門(mén)的負(fù)責(zé)人更多權(quán)力和更明晰的激勵(lì)措施。投資者為之雀躍:寶潔公司的股票三天內(nèi)上漲2.2%,,同期標(biāo)普500指數(shù)卻下跌3%,。首席執(zhí)行官泰勒稱(chēng)其為“公司過(guò)去20年中最重大的組織變革”。 |

With Immelt’s commitment trashed and their plan for GE now a shambles, Garden and Peltz stopped asking about a board seat and started demanding one. At that same time, Peltz happened to be demonstrating his ferociousness in the proxy fight with P&G. GE added Garden to its board in October, no proxy fight needed. From then until now, GE’s news has gone from bad to worse. Its most dramatic response has been the radical restructuring of the board, a process that began soon after Garden joined. Half the 18 directors left—an unprecedented putsch—and were replaced by three new directors, one of whom was Larry Culp. Speculation followed instantly: Was he the CEO in waiting? And if so, was Trian behind it? The firm won’t comment, but it issued a fact sheet about itself last May that observed that at GE, “three new directors joined the board including Larry Culp, former CEO of Danaher,” while omitting the names of the other two. Insiders say Culp disavowed any desire to be CEO—a sure sign the possibility existed. From Trian’s perspective, the GE board revamp was significant progress. More followed when Peltz took his seat on P&G’s board. The vitriol of the proxy fight had evaporated. “We respect Nelson Peltz … and look forward to his contributions as a member of P&G’s board,” Taylor said in a statement. Peltz said he was “l(fā)ooking forward to working closely” with Taylor. The first hint of Peltz-led change arrived in a July securities filing disclosing that P&G had revised its incentive pay plan for top managers, tying pay more closely to individual performance and less to corporate results. That was classic Peltz, followed in November by a far more significant change reorganizing the company into six units headed by chiefs with more power and clearer incentives. Investors cheered: P&G’s stock rose 2.2% over three days when the S&P 500 dropped 3%. CEO Taylor called it “the most significant organization change we’ve made in the last 20 years.” |

|

這是佩爾茨兩大藍(lán)籌股賭局的狀態(tài):寶潔一直在掙扎,,可能仍將繼續(xù)掙扎下去,。最近的結(jié)構(gòu)性重組會(huì)有所幫助,但寶潔的問(wèn)題更深層,。寶潔在國(guó)內(nèi)長(zhǎng)期外奉行建立大眾消費(fèi)品牌的戰(zhàn)略與如今消費(fèi)者越來(lái)越青睞小眾本土品牌的心理相悖,。例如,Harry’s和Dollar Shave Club的流行成功挑戰(zhàn)了吉列的市場(chǎng)地位,,讓寶潔公司大吃一驚,,這對(duì)于長(zhǎng)期引領(lǐng)市場(chǎng)的寶潔而言是全新的經(jīng)歷。更廣泛地說(shuō),,寶潔的文化可能會(huì)阻撓任何重大變化的出現(xiàn),。作為擁有181年歷史的公司,它或許會(huì)因?yàn)樘^(guò)古老而難以做出調(diào)整,。 寶潔公司還存在另外一個(gè)令佩爾茨不滿(mǎn)意的情況,。佩爾茨可以充當(dāng)催化劑,推動(dòng)公司緩慢改善,,避免出現(xiàn)災(zāi)難,,但會(huì)存在連續(xù)多年回報(bào)都十分微薄的情況。盡管如此,,一直以來(lái),,佩爾茨都甘愿花費(fèi)數(shù)年時(shí)間修復(fù)其他公司(比寶潔規(guī)模小得多),這些公司最終情況都出現(xiàn)好轉(zhuǎn),,恢復(fù)了強(qiáng)勢(shì)表現(xiàn),;Wendy's是過(guò)去十年中特里安的一場(chǎng)勝利,是一個(gè)正面例證,。至少還有希望,。 對(duì)通用電氣懷抱的任何希望都是佩爾茨2015年未實(shí)現(xiàn)愿景的部分殘留,。他的投資是一場(chǎng)巨賭,賭一家擁有120年歷史的工業(yè)公司能夠適應(yīng)由數(shù)字技術(shù)和相關(guān)服務(wù)引領(lǐng)的新時(shí)代,。這個(gè)想法沒(méi)錯(cuò),,但無(wú)論是通用電氣的高層還是特里安,沒(méi)有人能評(píng)估通用電氣的執(zhí)行能力,,結(jié)果證明它的執(zhí)行能力很糟糕,。此外,通用電氣和特里安因?yàn)槿蚴袌?chǎng)對(duì)發(fā)電渦輪機(jī)的需求急劇下滑被打得措手不及,。特里安的疏忽可以被原諒,,但通用電氣不能。之后,,通用電氣的全部投資者都因?yàn)楣緶u輪機(jī)業(yè)務(wù)和長(zhǎng)期護(hù)理保險(xiǎn)業(yè)務(wù)中存在的巨額負(fù)債被曝光而情緒失控,。回想起來(lái),,佩爾茨實(shí)在太過(guò)依賴(lài)伊梅爾特的保證了,。對(duì)一個(gè)表現(xiàn)一直不怎么樣的CEO充滿(mǎn)信任是個(gè)錯(cuò)誤。 從佩爾茨與通用電氣和寶潔公司合作的艱苦征程中,,可以勾畫(huà)出激進(jìn)主義的極限所在,。由于不持有控制性股權(quán),激進(jìn)投資者不能對(duì)公司的日常經(jīng)營(yíng)進(jìn)行管理,,這意味著他們總是離解決公司的深層文化問(wèn)題還有幾步之遙,,而在充滿(mǎn)顛覆的當(dāng)今時(shí)代,許多公司都深受文化困擾,。他們能期待的最佳方案是對(duì)首次執(zhí)行官的決策施加影響,。但真正做出轉(zhuǎn)變的決定權(quán)在首席執(zhí)行官手中,而不是激進(jìn)投資者,。這就是為什么他們的許多提案都是結(jié)構(gòu)性的,,大多是對(duì)公司進(jìn)行重組或分解。背后的邏輯在于,,新獨(dú)立的業(yè)務(wù)會(huì)因?yàn)榧?lì)措施更清晰,、復(fù)雜性減少、選擇增多而獲益,,這種策略通常都能奏效,。經(jīng)過(guò)特里安分解的大多數(shù)公司已經(jīng)證明,拆分后的公司更值錢(qián),。但這種戰(zhàn)略不利于維持偉大的具有悠久歷史的老公司。嚴(yán)酷的現(xiàn)實(shí)可能是,,在某個(gè)時(shí)刻,,它們將不再值得維持,。 佩爾茨押在美國(guó)商界兩大垂暮貴族身上的賭注繼續(xù)拖累著特里安的整體表現(xiàn)。現(xiàn)在最大的問(wèn)題是,,在佩爾茨實(shí)現(xiàn)了多年令人矚目的成功后,,這會(huì)是他職業(yè)生涯的轉(zhuǎn)折點(diǎn),抑或只是起起落落生意場(chǎng)上的一個(gè)低潮,。無(wú)論結(jié)果如何,,我們要清楚地看到,為了能在世界上最頑固最難修復(fù)的兩家公司身上創(chuàng)造奇跡,,以修復(fù)公司為生的佩爾茨和愛(ài)德·加登已經(jīng)投入了巨額賭注,。 |

So here’s the state of Peltz’s duo of big blue-chip bets. P&G has been a hell of a struggle and will likely remain one. The new reorganization is a helpful structural change, but P&G’s problems go deeper. A long-standing strategy based on building mass-market national and international brands is at odds with today’s consumers who increasingly favor smaller, niche, and local brands. The rise of Harry’s and Dollar Shave Club as successful challengers to Gillette, for example, caught P&G flat-footed—a new experience for the longtime alpha-dog company. More broadly, P&G’s culture could sabotage any significant change. At age 181, it may be too old to adjust. Peltz faces another unsatisfying scenario at P&G. He could be the catalyst for slow improvement, avoiding disaster but returning puny gains over many years. Nonetheless, Peltz has been willing to spend years fixing other companies (much smaller than P&G) that eventually turned around and came back stronger; Wendy’s, a Trian triumph over the past decade, is a good example. At least there’s hope. Any hope for GE is a shriveled remnant of what Peltz envisioned in 2015. His investment was a huge gamble on a 120-year-old industrial company adapting to a new world of digital technology and related services. It was the right idea, but no one at the top of GE or at Trian could evaluate GE’s ability to execute it, which turned out to be poor. In addition, GE and Trian were blindsided by a vertiginous plunge in global demand for electricity-generating turbines. Trian could be forgiven for missing it; GE couldn’t. And then all GE investors got crushed by revelations of mammoth liabilities in the company’s turbine business and long-term-care insurance business. In retrospect, Peltz relied way, way too much on Immelt’s assurances. Putting that much trust in a CEO who had underperformed up to then was a mistake. Peltz’s odyssey with GE and P&G outlines the limits of activism. As investors with non-controlling stakes, activists can’t run a company day-to-day, which means they’re always a couple of steps removed from solving the deep cultural problems afflicting many companies in an age of disruption. Influencing the choice of the CEO is about the best they can hope for. But the real transformation is in that person’s hands, not in the activists’. That’s why so many of their proposals are structural, mostly for reorganizing or breaking up the company. The logic is that newly liberated business will benefit from clearer incentives, less complexity, and more options, and that strategy has often worked. Most of the companies that Trian has broken up have proved more valuable in pieces. But it isn’t a strategy that preserves great old institutions. The hard reality may be that at a certain point, they aren’t worth preserving any longer. Peltz’s wager on the aging aristocracy of American business continues to wallop Trian’s performance. The great question now is whether this is a turning point for him after years of standout success or just a low point in a business full of ups and downs. As an answer plays out, the sobering truth is that he and Ed Garden, who fix companies for a living, have staked a great deal on working wonders at two of the most fix-resistant companies in the world. |

***

朝著錯(cuò)誤的方向前進(jìn)

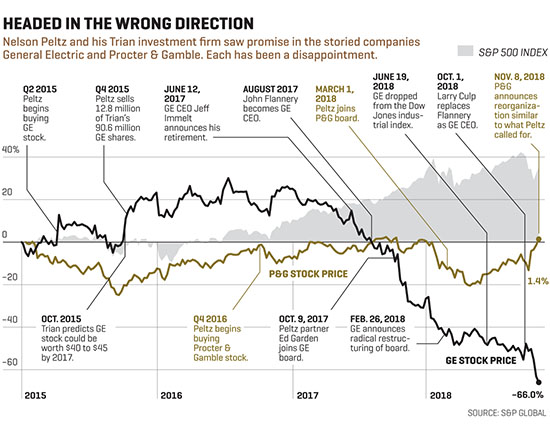

納爾遜·佩爾茨和他的特里安投資公司認(rèn)為著名的通用電氣和寶潔公司都有可觀(guān)前景。但兩家公司都令他失望了,。

2015年第二季度:佩爾茨開(kāi)始買(mǎi)入通用電氣股票,。

2015年10月:特里安預(yù)測(cè)通用電氣股價(jià)能在2017年達(dá)到40至45美元。

2015年第四季度:佩爾茨從特里安所持9060萬(wàn)美元通用電氣股票中出售1280萬(wàn),。

2016年第四季度:佩爾茨開(kāi)始買(mǎi)入寶潔股票,。

2017年6月12日:通用電氣首席執(zhí)行官杰夫·伊梅爾特宣布退休。

2017年8月:約翰·弗蘭納里出任通用電氣首席執(zhí)行官,。

2017年10月9日:佩爾茨合伙人加登進(jìn)入通用電氣董事會(huì),。

2018年2月26日:通用電氣宣布董事會(huì)洗牌。

2018年3月1日:佩爾茨加入寶潔董事會(huì),。

2018年6月19日:通用電氣被道瓊斯工業(yè)指數(shù)除名,。

2018年10月1日:拉里·卡爾普取代弗蘭納里成為通用電氣首席執(zhí)行官。

2018年11月8日:寶潔宣布類(lèi)似于佩爾茨提出的重組計(jì)劃,。

***

|

(財(cái)富中文網(wǎng)) 本文的另一個(gè)版本作為《2019年投資者指南》的一部分刊載于2018年12月1日的《財(cái)富》雜志,。 譯者:Agatha |

A version of this article appears in the December 1, 2018 issue of Fortune, as part of the “2019 Investor’s Guide.” |