美國人中青年面臨沉重財務(wù)壓力,,后悔沒有攢錢

JANE THIER

2023-08-11

Z世代和千禧一代對自己沒有積攢更多儲蓄而感到沮喪,。

文本設(shè)置

文本設(shè)置

Plus(0條)

Plus(0條)

這不僅僅是時不時犒勞自己一下。當(dāng)年輕人反思自己的消費決策時,,往往充滿了遺憾,。這一切所帶來的壓力確實讓他們不堪重負(fù)。

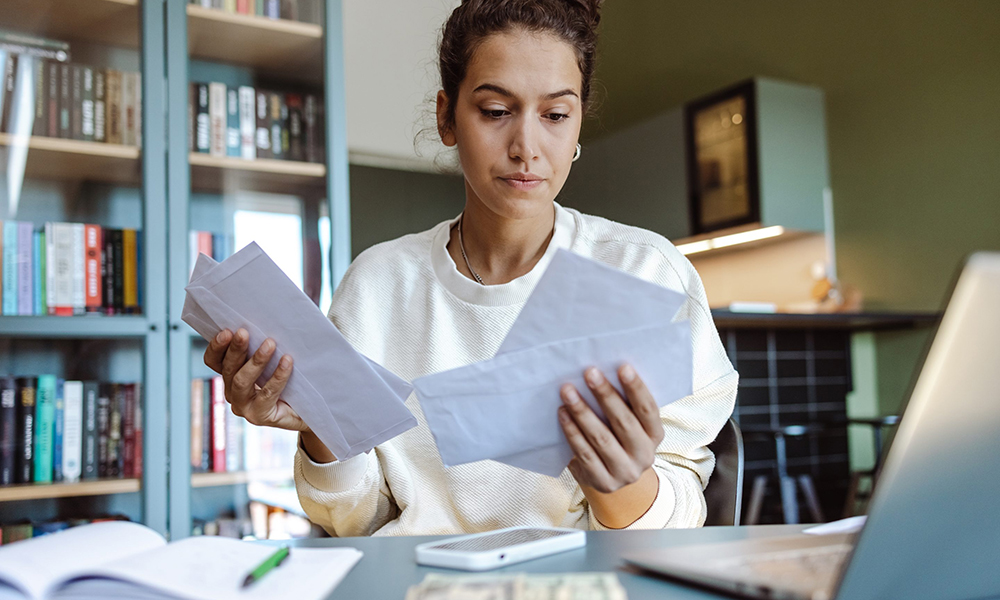

根據(jù)Bankrate最近對近3,700名成年人進(jìn)行的一項調(diào)查,,近四分之三的美國人在財務(wù)方面存在某種遺憾,。在心懷遺憾的Z世代和千禧一代中,分別有60%和57%的人表示,,今年的壓力比去年更大,,而X世代和嬰兒潮一代的這一比例分別為45%和38%。

千禧一代和Z世代在財務(wù)方面最后悔的事情是:沒有積攢足夠多的儲蓄以備不時之需(這一比例分別為21%和17%),。不足為奇的是:他們中的大多數(shù)人認(rèn)為,,如果今天失業(yè),他們將無法支付一個月的開銷,。

紐約人壽保險公司(New York Life)財務(wù)健康主管蘇珊娜·施密特(Suzanne Schmitt)在接受《財富》雜志采訪時表示,,在財務(wù)目標(biāo)方面,盡管一直以來所有年齡段的美國人都將建立應(yīng)急資金放在高度優(yōu)先的地位,,但年輕員工比年長員工更難實現(xiàn)這一目標(biāo),。由于嬰兒潮一代積累財富的時間較長,他們的應(yīng)急儲蓄賬戶明顯比千禧一代和Z世代的要充裕得多,。通常而言,,千禧一代的節(jié)儉程度不亞于他們的祖輩,但由于經(jīng)歷了兩次經(jīng)濟衰退,、一場疫情,、殘酷的房地產(chǎn)市場和歷史性的學(xué)生貸款債務(wù)危機,他們在成年期一直在努力積累財富,。超過30%的Z世代(面臨著同樣的經(jīng)濟挑戰(zhàn))根本沒有應(yīng)急儲蓄,。

建立應(yīng)急資金的需求與日俱增。多項研究發(fā)現(xiàn),,自疫情爆發(fā)以來,,超過半數(shù)的美國人表示,,如今建立應(yīng)急基金比以往任何時候都更加重要,他們現(xiàn)在負(fù)擔(dān)不起1000美元的緊急支出,。

不過,,這并不是千禧一代和Z世代在財務(wù)方面的唯一遺憾。對于這兩個年齡段的人來說,,“背負(fù)太多的信用卡債務(wù)”是他們的第二大遺憾,,其次是千禧一代“沒有足夠早地為退休儲蓄”,以及Z世代“背負(fù)太多學(xué)生貸款債務(wù)”,。

每個人都更關(guān)心自己的儲蓄,,而不是債務(wù)

Bankrate的首席金融分析師格雷格·麥克布萊德(Greg McBride)在報告中寫道,盡管債務(wù)和利率不斷攀升,,但與債務(wù)相關(guān)的遺憾相比,,儲蓄相關(guān)的遺憾更大。比起多還抵押貸款,、教育相關(guān)貸款或信用卡,,未能積攢足夠多的儲蓄更讓美國人痛心疾首。

總體而言,,在接受調(diào)查的成年人中,,大量對財務(wù)狀況感到遺憾的人表示,他們最大的遺憾是在職業(yè)生涯早期忽視了退休儲蓄(21%),,其次是背負(fù)了太多的信用卡債務(wù)(15%),以及沒有為緊急支出積攢足夠多的儲蓄 (14%),。嬰兒潮一代和X世代比年輕一代更有可能后悔沒有為退休積攢足夠多的儲蓄,,考慮到他們目前處于或即將進(jìn)入退休階段,這也是合乎情理的,。

但考慮到嬰兒潮一代享受到更強勁的經(jīng)濟帶來的紅利,,即使是他們也覺得自己的退休儲蓄不夠,那么,,這對年輕一代來說可能是個糟糕的信號,,因為他們通往財務(wù)獨立的道路要艱難得多。(近80%的年輕員工仍然依賴嬰兒潮一代的父母賺錢,。)

專家稱,,攢100萬美元退休已經(jīng)不夠了,美國人對這一點深有體會,。貝萊德(BlackRock)的一份報告顯示,,自2021年以來,對自己能否在退休后安享晚年沒有信心的員工比例增加了一倍多(從10%增至24%),。Z世代最不自信,。

理財規(guī)劃師查理·帕斯特(Charlie Pastor)對《財富》雜志的艾麗西亞·亞當(dāng)奇克(Alicia Adamczyk)表示:“隨著Z世代步入青年期,,新冠疫情的爆發(fā)嚴(yán)重影響了經(jīng)濟。老一輩人應(yīng)該明白,,下一代儲蓄者在短時間內(nèi)經(jīng)歷了很多經(jīng)濟動蕩,。”考慮到創(chuàng)紀(jì)錄的利率,、成千上萬的員工被解雇,,以及擁有房產(chǎn)或擺脫學(xué)生貸款債務(wù)的可能性越來越小,上述說法可能是輕描淡寫,。然而,,正如Bankrate所發(fā)現(xiàn)的那樣,錯失良機的遺憾仍然揮之不去,。

麥克布萊德解釋說:“隨著時間的推移,,復(fù)利有可能讓先前沒有積攢儲蓄的人更為痛心疾首,因為'本來有機會'實現(xiàn)的財務(wù)目標(biāo)與現(xiàn)實形成鮮明的對比,。以保守的6.5%的年回報率計算,,你在20多歲時存的每一美元,到退休時就會變成17美元,?!彼a充說,換句話說,,你在20多歲時沒有投資的每一美元,,“都變成在退休后無法拿到的17美元?!?/p>

但是,,盡管年輕員工的積蓄較少,他們?nèi)栽谂Υ蛳聢詫嵉幕A(chǔ),。在2021年,,Z世代員工比處于同年齡段的老一輩員工更有可能投資于公司的退休金計劃。這表明 Z 世代比他們自認(rèn)為的更有遠(yuǎn)見,。(財富中文網(wǎng))

譯者:中慧言-王芳

這不僅僅是時不時犒勞自己一下,。當(dāng)年輕人反思自己的消費決策時,往往充滿了遺憾,。這一切所帶來的壓力確實讓他們不堪重負(fù),。

根據(jù)Bankrate最近對近3,700名成年人進(jìn)行的一項調(diào)查,近四分之三的美國人在財務(wù)方面存在某種遺憾,。在心懷遺憾的Z世代和千禧一代中,,分別有60%和57%的人表示,今年的壓力比去年更大,,而X世代和嬰兒潮一代的這一比例分別為45%和38%,。

千禧一代和Z世代在財務(wù)方面最后悔的事情是:沒有積攢足夠多的儲蓄以備不時之需(這一比例分別為21%和17%),。不足為奇的是:他們中的大多數(shù)人認(rèn)為,如果今天失業(yè),,他們將無法支付一個月的開銷,。

紐約人壽保險公司(New York Life)財務(wù)健康主管蘇珊娜·施密特(Suzanne Schmitt)在接受《財富》雜志采訪時表示,在財務(wù)目標(biāo)方面,,盡管一直以來所有年齡段的美國人都將建立應(yīng)急資金放在高度優(yōu)先的地位,,但年輕員工比年長員工更難實現(xiàn)這一目標(biāo)。由于嬰兒潮一代積累財富的時間較長,,他們的應(yīng)急儲蓄賬戶明顯比千禧一代和Z世代的要充裕得多,。通常而言,千禧一代的節(jié)儉程度不亞于他們的祖輩,,但由于經(jīng)歷了兩次經(jīng)濟衰退,、一場疫情、殘酷的房地產(chǎn)市場和歷史性的學(xué)生貸款債務(wù)危機,,他們在成年期一直在努力積累財富,。超過30%的Z世代(面臨著同樣的經(jīng)濟挑戰(zhàn))根本沒有應(yīng)急儲蓄。

建立應(yīng)急資金的需求與日俱增,。多項研究發(fā)現(xiàn),,自疫情爆發(fā)以來,超過半數(shù)的美國人表示,,如今建立應(yīng)急基金比以往任何時候都更加重要,,他們現(xiàn)在負(fù)擔(dān)不起1000美元的緊急支出。

不過,,這并不是千禧一代和Z世代在財務(wù)方面的唯一遺憾,。對于這兩個年齡段的人來說,“背負(fù)太多的信用卡債務(wù)”是他們的第二大遺憾,,其次是千禧一代“沒有足夠早地為退休儲蓄”,,以及Z世代“背負(fù)太多學(xué)生貸款債務(wù)”,。

每個人都更關(guān)心自己的儲蓄,,而不是債務(wù)

Bankrate的首席金融分析師格雷格·麥克布萊德(Greg McBride)在報告中寫道,盡管債務(wù)和利率不斷攀升,,但與債務(wù)相關(guān)的遺憾相比,,儲蓄相關(guān)的遺憾更大。比起多還抵押貸款,、教育相關(guān)貸款或信用卡,,未能積攢足夠多的儲蓄更讓美國人痛心疾首。

總體而言,,在接受調(diào)查的成年人中,,大量對財務(wù)狀況感到遺憾的人表示,,他們最大的遺憾是在職業(yè)生涯早期忽視了退休儲蓄(21%),其次是背負(fù)了太多的信用卡債務(wù)(15%),,以及沒有為緊急支出積攢足夠多的儲蓄 (14%),。嬰兒潮一代和X世代比年輕一代更有可能后悔沒有為退休積攢足夠多的儲蓄,考慮到他們目前處于或即將進(jìn)入退休階段,,這也是合乎情理的,。

但考慮到嬰兒潮一代享受到更強勁的經(jīng)濟帶來的紅利,即使是他們也覺得自己的退休儲蓄不夠,,那么,,這對年輕一代來說可能是個糟糕的信號,因為他們通往財務(wù)獨立的道路要艱難得多,。(近80%的年輕員工仍然依賴嬰兒潮一代的父母賺錢,。)

專家稱,攢100萬美元退休已經(jīng)不夠了,,美國人對這一點深有體會,。貝萊德(BlackRock)的一份報告顯示,自2021年以來,,對自己能否在退休后安享晚年沒有信心的員工比例增加了一倍多(從10%增至24%),。Z世代最不自信。

理財規(guī)劃師查理·帕斯特(Charlie Pastor)對《財富》雜志的艾麗西亞·亞當(dāng)奇克(Alicia Adamczyk)表示:“隨著Z世代步入青年期,,新冠疫情的爆發(fā)嚴(yán)重影響了經(jīng)濟,。老一輩人應(yīng)該明白,下一代儲蓄者在短時間內(nèi)經(jīng)歷了很多經(jīng)濟動蕩,?!笨紤]到創(chuàng)紀(jì)錄的利率、成千上萬的員工被解雇,,以及擁有房產(chǎn)或擺脫學(xué)生貸款債務(wù)的可能性越來越小,,上述說法可能是輕描淡寫。然而,,正如Bankrate所發(fā)現(xiàn)的那樣,,錯失良機的遺憾仍然揮之不去。

麥克布萊德解釋說:“隨著時間的推移,,復(fù)利有可能讓先前沒有積攢儲蓄的人更為痛心疾首,,因為'本來有機會'實現(xiàn)的財務(wù)目標(biāo)與現(xiàn)實形成鮮明的對比。以保守的6.5%的年回報率計算,,你在20多歲時存的每一美元,,到退休時就會變成17美元。”他補充說,,換句話說,,你在20多歲時沒有投資的每一美元,“都變成在退休后無法拿到的17美元,?!?/p>

但是,盡管年輕員工的積蓄較少,,他們?nèi)栽谂Υ蛳聢詫嵉幕A(chǔ),。在2021年,Z世代員工比處于同年齡段的老一輩員工更有可能投資于公司的退休金計劃,。這表明 Z 世代比他們自認(rèn)為的更有遠(yuǎn)見,。(財富中文網(wǎng))

譯者:中慧言-王芳

It’s more than just a little treat here and there. When young adults reflect on their spending decisions, they’re filled with regret. And the stress about it all is really, really getting to them.

Nearly three-quarters of Americans have some type of financial regret, according to a recent Bankrate survey of nearly 3,700 adults. For the Gen Zers and millennials who feel this way, 60% and 57%, respectively, say it’s stressing them out more this year than last year—compared to just 45% of Gen Xers and 38% of baby boomers.

At the top of both millennials’ and Gen Zers’ financial regrets: not socking away enough money for emergency expenses (at 21% and 17%, respectively). No wonder; most of them think they’re unable to pay one month of expenses if they lost their job today.

While funding an emergency account has long been a “high-priority financial goal” for Americans of all ages, younger workers struggle more to meet that goal than older workers, Suzanne Schmitt, head of financial wellness at New York Life, told Fortune. Because they’ve had a longer time to build wealth, boomers’ emergency savings accounts are significantly beefier than those of millennials and Gen Zers. Millennials, generally no less frugal than their forebears, have spent their adulthood struggling to build wealth thanks to two recessions, a pandemic, an unforgiving housing market, and a historic student debt crisis. And over 30% of Gen Zers, who have also had their fair share of economic challenges, have no emergency savings at all.

The need for an emergency fund is growing. Several studies have found that since the pandemic, over half of Americans say an emergency fund is more crucial now than ever before and that they wouldn’t be able to afford an emergency $1,000 expense right now.

It’s not millennials’ and Gen Z’s only financial regret, though. For both age groups, “taking on too much credit card debt” was their second-place regret, followed by “not saving for retirement early enough” for millennials and “taking on too much student debt” for Gen Zers.

Everyone is more concerned about their savings than their debt

Despite mounting debt and interest rates, savings-related regrets continue to outpace debt-related regrets, Greg McBride, Bankrate’s chief financial analyst, wrote in the report. Failing to save enough money weighed more on Americans’ conscience than overpaying on their mortgage, education, or credit card purchases.

Overall, the largest share of adults surveyed with a financial regret said their biggest one is neglecting to save for retirement earlier on in their careers (21%), followed by taking on too much credit card debt (15%), and failing to save sufficient money for emergency expenses (14%). Boomers and Gen X were more likely than younger generations to regret not saving enough for retirement, which makes sense considering that’s the life stage they’re currently in or approaching.

But when you consider that boomers benefited from a stronger economy, the fact that even they feel their retirement savings aren’t enough might be a bad sign for younger generations, whose on-ramp to financial independence has been infinitely more fraught. (Nearly 80% of young workers still rely on their boomer parents for money.)

Experts say $1 million is no longer enough to retire, and Americans are feeling it. The share of workers who don’t feel confident that they’ll ever be able to comfortably retire—period—has more than doubled (from 10% to 24%) since 2021, per a BlackRock report. Gen Zers felt the least confident.

“The onset of the COVID-19 pandemic rocked the economy as Gen Z entered young adulthood,” Charlie Pastor, a financial planner, told Fortune’s Alicia Adamczyk. “Older generations should understand that the next generation of savers has seen a lot of economic turbulence in a short period of time.” Between historic interest rates, hundreds of thousands of layoffs, and the ever-vanishing possibility of owning property or escaping student debt, that may be an understatement. Yet, as Bankrate finds, the regrets over missed opportunities still linger.

“The power of compounding has the potential to magnify regrets about foregone savings over time as a ‘what could have been’ realization becomes more stark,” McBride explained. “At a modest 6.5% annual return, every dollar you put away in your twenties becomes $17 by the time you retire.” Put another way, McBride added, every dollar you don’t invest in your twenties “is $17 you won’t have in retirement.”

But young workers, despite having less saved up, are nonetheless working to build a solid foundation. Gen Z workers were more likely to invest in their company’s retirement plan than colleagues in older generations were at their age in 2021. That suggests Gen Z is more future-minded than they give themselves credit for.

請打開財富Plus APP