高盛大膽預(yù)測,,美國房價將于年中觸底

LANCE LAMBERT

2023-02-08

雖然高盛預(yù)測2023年全美房價將下跌2.6%,但并非美國市場都如此幸運,。

文本設(shè)置

文本設(shè)置

Plus(0條)

Plus(0條)

美國房地產(chǎn)市場可能正在接近最低點。至少高盛(Goldman Sachs)這樣認(rèn)為,。

兩周前,,投資銀行高盛才在一篇名為《在好轉(zhuǎn)之前會先變得更糟》(Getting Worse Before Getting Better)的報告中,下調(diào)了對美國房地產(chǎn)市場的展望評級,,但在2023年1月23日發(fā)表的一篇名為《2023年房地產(chǎn)市場展望:尋找谷底》(2023 Housing Outlook: Finding a Trough)的文章中卻改變了立場,。

該投行的研究人員推翻了1月10日對美國房價2023年下跌6.1%的預(yù)測,而是認(rèn)為,,到2023年底,,美國全國房價將僅下跌2.6%。

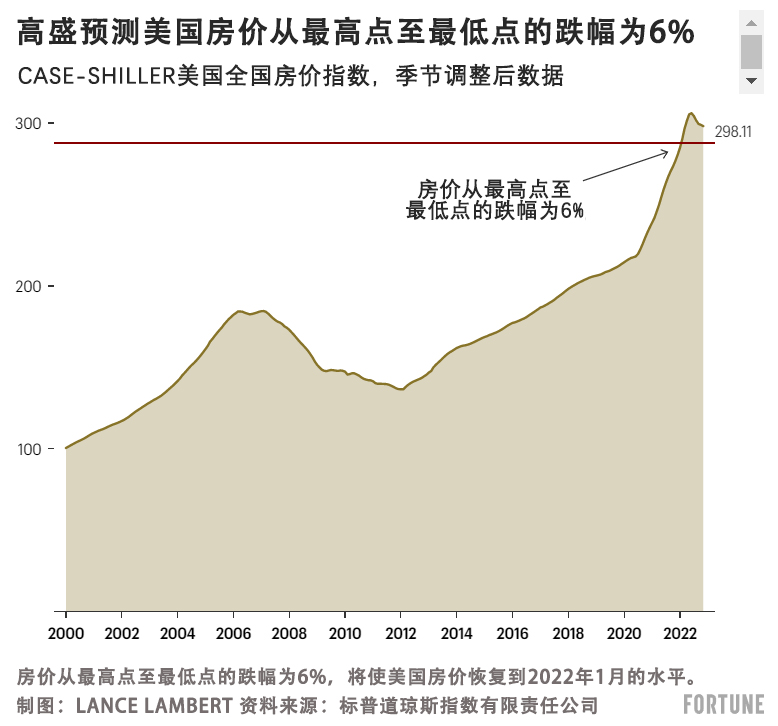

高盛表示,,今年夏天美國房價將觸底,,全國房價將較2022年6月的最高點下跌約6%。高盛研究人員此前曾預(yù)測,,美國房價從最高點至最低點的跌幅更接近10%,。

研究人員表示:“我們預(yù)測,全美房價從最高點至最低點的跌幅約為6%,,在年中前后,,房價會停止下跌。對于區(qū)域市場,,我們預(yù)測太平洋海岸和西南地區(qū)的房價降幅更大,,這些地區(qū)的平均房屋存量增幅最大,而在大西洋中部和中西部地區(qū)房價跌幅較小,,過去兩年,,這些地區(qū)的房價可負(fù)擔(dān)性更高?!?/p>

高盛為何會向上修正房價預(yù)測,?高盛表示,最近的數(shù)據(jù)表明購房人需求回升,。

研究人員表示:“房屋銷量似乎出現(xiàn)增長的勢頭,。1月到目前為止,平均抵押貸款購房申請量比去年10月低谷時期增長了9%,,而基于調(diào)查的購房意愿指標(biāo)顯著反彈,?!?/p>

為了更明確地了解全美和地區(qū)房價的未來走向,《財富》雜志向高盛索要了完整預(yù)測,。

讓我們看看高盛的研究結(jié)果,。

與畢馬威(KPMG)不同,高盛預(yù)測美國房價回調(diào)幅度不會達(dá)到兩位數(shù),。高盛表示,,在當(dāng)前的市場周期不會出現(xiàn)更大幅度的房價回調(diào),原因有三,。

研究人員寫道:“首先,,過去兩年快速增長的未使用房屋凈值意味著,即使房價下跌幅度超出我們的預(yù)期,,也只有一小部分抵押貸款人會遭遇虧損,。其次,超過90%的未償還抵押貸款為固定利率貸款,,這意味著利率上漲不會導(dǎo)致大多數(shù)業(yè)主的償債成本大幅增加,。第三,美國家庭財務(wù)狀況依舊強勁,,整體杠桿率較低,,并且在新冠疫情期間家庭積累了大量儲蓄?!?/p>

高盛表示,,這三個因素應(yīng)該可防止發(fā)生“層疊違約,層疊違約曾導(dǎo)致全球金融危機之后美國房價下跌,?!?007年至2008年全球金融危機(GFC)之后,美國房價回調(diào),,從2007年至2012年美國房價下跌26%,,是高盛預(yù)測的目前從最高點至最低點的6%跌幅的四倍以上。

雖然高盛預(yù)測2023年全美房價將下跌2.6%,,但并非美國市場都如此幸運。

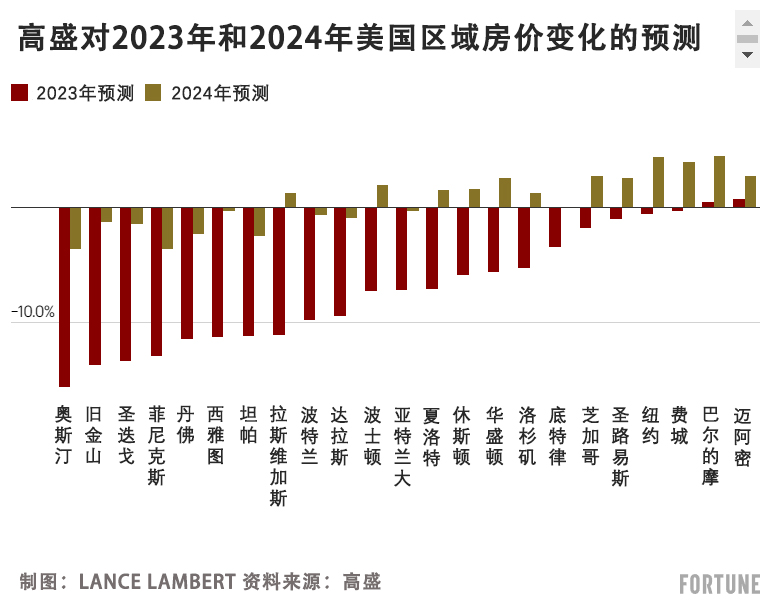

2023年,,高盛預(yù)測多個過熱的市場房價會出現(xiàn)兩位數(shù)下跌,,包括奧斯汀(-16%),、舊金山(-14%),、圣地亞哥(-13%)、菲尼克斯(-13%),、丹佛(-11%),、西雅圖(-11%)、坦帕(-11%)和拉斯維加斯(-11%)。好消息是,,高盛預(yù)測巴爾的摩(+0.5%)和邁阿密(+0.8%)等市場的房價將會上漲,。

高盛研究人員在最新報告中寫道:“城市房地產(chǎn)市場的趨勢將取決于房屋供需關(guān)系。在芝加哥和費城等可負(fù)擔(dān)性更強的大都市,,新抵押貸款的還款成本僅占月收入的約四分之一,,這些市場的房價跌幅將低于可負(fù)擔(dān)性較差的西部城市,因為這些城市的抵押貸款還款成本占月收入的四分之三,?!?/p>

在抵押貸款利率方面,高盛表示購房人不應(yīng)指望有好消息,。該投行預(yù)測,,到2023年年底,30年期固定抵押貸款平均利率將上浮至6.5%,。截至周四,,30年期固定抵押貸款平均利率為6.09%。(財富中文網(wǎng))

譯者:劉進龍

審校:汪皓

美國房地產(chǎn)市場可能正在接近最低點,。至少高盛(Goldman Sachs)這樣認(rèn)為,。

兩周前,投資銀行高盛才在一篇名為《在好轉(zhuǎn)之前會先變得更糟》(Getting Worse Before Getting Better)的報告中,,下調(diào)了對美國房地產(chǎn)市場的展望評級,,但在2023年1月23日發(fā)表的一篇名為《2023年房地產(chǎn)市場展望:尋找谷底》(2023 Housing Outlook: Finding a Trough)的文章中卻改變了立場。

該投行的研究人員推翻了1月10日對美國房價2023年下跌6.1%的預(yù)測,,而是認(rèn)為,,到2023年底,美國全國房價將僅下跌2.6%,。

高盛表示,,今年夏天美國房價將觸底,全國房價將較2022年6月的最高點下跌約6%,。高盛研究人員此前曾預(yù)測,,美國房價從最高點至最低點的跌幅更接近10%。

研究人員表示:“我們預(yù)測,,全美房價從最高點至最低點的跌幅約為6%,,在年中前后,房價會停止下跌,。對于區(qū)域市場,,我們預(yù)測太平洋海岸和西南地區(qū)的房價降幅更大,這些地區(qū)的平均房屋存量增幅最大,,而在大西洋中部和中西部地區(qū)房價跌幅較小,,過去兩年,,這些地區(qū)的房價可負(fù)擔(dān)性更高?!?/p>

高盛為何會向上修正房價預(yù)測,?高盛表示,最近的數(shù)據(jù)表明購房人需求回升,。

研究人員表示:“房屋銷量似乎出現(xiàn)增長的勢頭,。1月到目前為止,平均抵押貸款購房申請量比去年10月低谷時期增長了9%,,而基于調(diào)查的購房意愿指標(biāo)顯著反彈,。”

為了更明確地了解全美和地區(qū)房價的未來走向,,《財富》雜志向高盛索要了完整預(yù)測,。

讓我們看看高盛的研究結(jié)果。

與畢馬威(KPMG)不同,,高盛預(yù)測美國房價回調(diào)幅度不會達(dá)到兩位數(shù),。高盛表示,在當(dāng)前的市場周期不會出現(xiàn)更大幅度的房價回調(diào),,原因有三,。

研究人員寫道:“首先,過去兩年快速增長的未使用房屋凈值意味著,,即使房價下跌幅度超出我們的預(yù)期,,也只有一小部分抵押貸款人會遭遇虧損。其次,,超過90%的未償還抵押貸款為固定利率貸款,,這意味著利率上漲不會導(dǎo)致大多數(shù)業(yè)主的償債成本大幅增加。第三,,美國家庭財務(wù)狀況依舊強勁,,整體杠桿率較低,并且在新冠疫情期間家庭積累了大量儲蓄,?!?/p>

高盛表示,這三個因素應(yīng)該可防止發(fā)生“層疊違約,,層疊違約曾導(dǎo)致全球金融危機之后美國房價下跌,。”2007年至2008年全球金融危機(GFC)之后,,美國房價回調(diào),從2007年至2012年美國房價下跌26%,,是高盛預(yù)測的目前從最高點至最低點的6%跌幅的四倍以上,。

雖然高盛預(yù)測2023年全美房價將下跌2.6%,,但并非美國市場都如此幸運。

2023年,,高盛預(yù)測多個過熱的市場房價會出現(xiàn)兩位數(shù)下跌,,包括奧斯汀(-16%),、舊金山(-14%),、圣地亞哥(-13%)、菲尼克斯(-13%),、丹佛(-11%),、西雅圖(-11%)、坦帕(-11%)和拉斯維加斯(-11%),。好消息是,,高盛預(yù)測巴爾的摩(+0.5%)和邁阿密(+0.8%)等市場的房價將會上漲。

高盛研究人員在最新報告中寫道:“城市房地產(chǎn)市場的趨勢將取決于房屋供需關(guān)系,。在芝加哥和費城等可負(fù)擔(dān)性更強的大都市,,新抵押貸款的還款成本僅占月收入的約四分之一,這些市場的房價跌幅將低于可負(fù)擔(dān)性較差的西部城市,,因為這些城市的抵押貸款還款成本占月收入的四分之三,。”

在抵押貸款利率方面,,高盛表示購房人不應(yīng)指望有好消息,。該投行預(yù)測,到2023年年底,,30年期固定抵押貸款平均利率將上浮至6.5%,。截至周四,30年期固定抵押貸款平均利率為6.09%,。(財富中文網(wǎng))

譯者:劉進龍

審校:汪皓

The U.S. housing market might finally be nearing the bottom. At least that’s according to Goldman Sachs.

Just two weeks after Goldman Sachs downgraded its outlook for the U.S. housing market in a paper titled Getting Worse Before Getting Better, the investment bank reversed course on Jan. 23 in a paper titled 2023 Housing Outlook: Finding a Trough.

Instead of U.S. home prices falling 6.1% in 2023, which was their Jan. 10 prediction, researchers at the investment bank now expect national home prices to end 2023 down just 2.6%.

By the time U.S. home prices bottom out this summer, Goldman Sachs says, national home prices will be down around 6% from its June 2022 peak. Previously, Goldman Sachs researchers were expecting that peak-to-trough decline to come in closer to 10%.

“We expect a peak-to-trough decline in national home prices of roughly 6% and for prices to stop declining around midyear. On a regional basis, we project larger declines across the Pacific Coast and Southwest regions—which have seen the largest increases in inventory on average—and more modest declines across the Mid-Atlantic and Midwest—which have maintained greater affordability over the past couple years,” wrote the researchers.

Why the upward revision? Recent data, Goldman Sachs says, points to an uptick in homebuyer demand.

“Home sales appear set to turn higher. Mortgage purchase applications have averaged 9% above their October trough so far in January, and survey-based measures of purchasing intentions have rebounded sharply,” wrote Goldman Sachs researchers.

To get a better idea of where both national and regional home prices might be headed, Fortune asked Goldman Sachs to provide us with its full forecast.

Let’s take a look.

Unlike KPMG, Goldman Sachs does not expect a double-digit home price correction. The investment bank says there are three reasons why a steeper correction won't happen this cycle.

"First, the rapid buildup of untapped home equity over the last couple years means that even if prices declined more sharply than we expect, only a small share of mortgage borrowers would be underwater," wrote Goldman Sachs researchers. "Second, over 90% of outstanding mortgages are fixed rate, meaning that the rise in interest rates will not lead to a spike in debt service costs for most homeowners. And third, household balance sheets remain strong, with low aggregate leverage and considerable remaining pent-up savings from the COVID-19 pandemic."

Those three factors, Goldman Sachs says, should prevent the potential "for the cascading defaults that contributed to the post-GFC drawdown." That previous correction—after the 2007–2008 Global Financial Crisis (GFC), which saw U.S. home prices fall 26% between 2007 and 2012—is four times greater than the 6% peak-to-trough decline Goldman Sachs is predicting this time around.

While Goldman Sachs expects national home prices to fall 2.6% in 2023, not every market will be so lucky.

In 2023, Goldman Sachs expects double-digit home price declines only in overheated markets like Austin (-16%), San Francisco (-14%), San Diego (-13%), Phoenix (-13%), Denver (-11%), Seattle (-11%), Tampa (-11%), and Las Vegas (-11%). On the positive side, Goldman Sachs expects home prices will rise in markets like Baltimore (+0.5%) and Miami (+0.8%).

"Metro-level trends will be dictated by a tug-of-war between housing demand and supply. MSAs [metros] with stronger affordability like Chicago and Philadelphia—for which payments on new mortgages only cost roughly a quarter of monthly income—should see smaller home price declines than metros with poor affordability like many cities in the West—some of which are seeing mortgage payments claim three-quarters of monthly income," wrote Goldman Sachs researchers in their latest note.

On the mortgage rate front, Goldman Sachs says buyers shouldn't expect much relief. By the end of 2023, the investment bank expects the average 30-year fixed mortgage rate will tick back up to 6.5%. As of Thursday, the average 30-year fixed mortgage rate sits at 6.09%.

請打開財富Plus APP